Nelson Nash: Pioneer of the Infinite Banking Concept

R. Nelson Nash, born in 1931, revolutionized personal finance with his development of the Infinite Banking Concept (IBC). This innovative approach challenges traditional financial wisdom by advocating the use of dividend-paying whole life insurance as a personal banking system. Nash’s ideas have empowered countless individuals to take control of their financial futures and build lasting wealth.

The Life of Nelson Nash

Early Years and Education

Robert Nelson Nash was born on March 15, 1931, in Greene County, Georgia. He grew up in Athens, Georgia, where he developed a strong work ethic and a curiosity about finance. Nash graduated from the University of Georgia with a B.S. in Forestry in 1952, a background that would later influence his financial thinking, particularly regarding compound interest over long periods.

Military Service and Career Transitions

Following graduation, Nash served two years in the U.S. Air Force (1952-1954) as an aerial photo interpreter. He later joined the North Carolina Army National Guard as a fixed-wing pilot, eventually earning Master Aviator Wings over a 30-year military career.

Nash’s professional life saw several transitions. He worked as a forestry consultant in North Carolina for nine years before moving to Birmingham, Alabama, in 1963 to continue his forestry work. In 1964, Nash made a pivotal career change, entering the life insurance business – a decision that would ultimately lead to the development of the Infinite Banking Concept.

Personal Life

Throughout his life, Nash was devoted to his family. He was married to Mary Edwards Williams for 66 years until his passing in 2019. Together, they raised three children: Debby, Barrington, and Kimberly.

Nelson Nash’s Faith and Finance

Nelson Nash’s approach to finance was deeply intertwined with his Christian faith. His religious beliefs played a significant role in shaping his financial philosophy and the development of the Infinite Banking Concept (IBC).

Biblical Financial Principles

Nash often referred to biblical principles in his teachings about finance. He believed that the Bible offered timeless wisdom about money management, stewardship, and the ethical use of resources. For Nash, the concept of becoming your own banker aligned with the biblical principle of good stewardship – making the most of the resources one has been given.

The Moral Dimension of Finance

Nash viewed finance not just as a mathematical or economic issue, but as a moral one. He believed that the traditional banking system often led people into debt and financial bondage, a state he saw as contrary to biblical teachings. In contrast, he saw IBC as a way to achieve financial freedom and independence, aligning with his interpretation of biblical financial wisdom.

Stewardship and Legacy

The idea of leaving a legacy, which is central to IBC, was also influenced by Nash’s religious views. He often spoke about the importance of generational wealth transfer, not just in financial terms, but as a way of passing on values and financial wisdom to future generations. This aligns with the biblical concept of leaving an inheritance for one’s children and grandchildren.

Faith-Based Teaching Style

Nash’s teaching style, characterized by its conversational tone and use of parables and real-life examples, was reminiscent of biblical teaching methods. He often used stories and analogies to explain complex financial concepts, much like the parables found in the Bible.

Ethical Considerations

Nash’s emphasis on ethical financial practices was rooted in his Christian beliefs. He was critical of what he saw as manipulative or exploitative financial practices and advocated for a more transparent and equitable approach to personal finance.

Community and Mutual Support

While IBC is primarily focused on individual financial management, Nash’s Christian background also influenced his views on community and mutual support. He encouraged the sharing of knowledge and resources within communities, reflecting the Christian principle of mutual care and support.

Contentment and Financial Peace

Nash often spoke about the importance of contentment and finding peace in one’s financial life. This perspective was deeply rooted in his Christian faith, which emphasized finding fulfillment beyond material wealth.

The Birth of the Infinite Banking Concept

Nash’s experience as a life insurance agent, spanning over 35 years, provided him with unique insights into the financial industry. He worked with prestigious companies like The Equitable Life Assurance Society of the U.S. and Guardian, earning numerous accolades.

Nash’s experience as a life insurance agent, spanning over 35 years, provided him with unique insights into the financial industry. He worked with prestigious companies like The Equitable Life Assurance Society of the U.S. and Guardian, earning numerous accolades.

However, it was Nash’s personal experiences, particularly in real estate investing, that led to the development of IBC. In the early 1980s, Nash found himself struggling with high interest rates on his real estate investments. This financial pressure, combined with his knowledge of life insurance and his forestry background, led to the insight that would become the Infinite Banking Concept.

Over 20 years, Nash refined his ideas, testing them in his own life and observing their effectiveness. The culmination of Nash’s financial philosophy came in 2000 with the publication of his seminal work, “Becoming Your Own Banker,” which introduced the Infinite Banking Concept to a wider audience.

The Austrian Economics Foundation of Nash’s Philosophy

Nelson Nash’s development of the Infinite Banking Concept was heavily influenced by the principles of Austrian Economics. This school of economic thought provided the theoretical underpinning for many of Nash’s ideas about money, banking, and personal finance.

Key Principles of Austrian Economics in Nash’s Work

- Subjective Theory of Value: Austrian Economics emphasizes that the value of goods and services is subjective, determined by individual preferences rather than intrinsic worth. Nash applied this principle to his critique of traditional financial planning, arguing that individuals should have more control over their financial decisions based on their personal values and goals.

- Time Preference: The Austrian concept of time preference, which states that individuals prefer present goods over future goods, influenced Nash’s approach to long-term financial planning. IBC encourages individuals to think in terms of long-term wealth building, challenging the short-term thinking often prevalent in personal finance.

- Capital Theory: Austrian Economics views capital as a structure of heterogeneous goods used in production. Nash’s concept of using whole life insurance as a personal banking system reflects this idea of capital as a tool for creating future wealth.

- Criticism of Fractional Reserve Banking: Austrian economists are critical of fractional reserve banking, viewing it as a source of economic instability. Nash shared this view, which formed a key part of his critique of the traditional banking system and his advocacy for becoming your own banker.

- Business Cycle Theory: The Austrian theory of the business cycle, which attributes economic booms and busts to monetary expansion by central banks, informed Nash’s skepticism of traditional financial institutions and his emphasis on personal financial sovereignty.

- Entrepreneurship: Austrian Economics places a strong emphasis on entrepreneurship as a driving force in the economy. Nash’s IBC encourages individuals to think like entrepreneurs in managing their personal finances, taking control and making strategic decisions.

Austrian Economists Who Influenced Nash

Nash was particularly influenced by several prominent Austrian economists:

- Ludwig von Mises: Nash often cited Mises’ work, especially his critiques of central banking and fiat currency.

- Friedrich Hayek: Hayek’s ideas on the decentralization of knowledge and the importance of individual decision-making in complex systems resonated with Nash’s approach to personal finance.

- Murray Rothbard: Rothbard’s criticisms of fractional reserve banking and advocacy for a 100% reserve gold standard influenced Nash’s thinking on the nature of money and banking.

- Hernando de Soto: While not strictly an Austrian economist, de Soto’s work on the importance of property rights and formalizing “dead capital” aligns with Nash’s IBC. De Soto’s emphasis on leveraging assets and creating systems that empower individuals economically parallels Nash’s approach of using whole life insurance as a formal, accessible way to store and grow personal capital.

Nelson Nash’s Critique of the Traditional Banking System

Nelson Nash’s development of the Infinite Banking Concept was deeply rooted in his critical view of the traditional banking system. His perspective was shaped by his study of Austrian Economics and his personal experiences with the financial industry.

The Parasitic Nature of Banking

Nash viewed the traditional banking system as inherently parasitic. He argued that banks, by their very nature, extract wealth from individuals and businesses without providing commensurate value. In his view, every time a person takes out a loan or uses a credit card, they’re feeding into a system that primarily benefits the banks rather than the individual.

Fractional Reserve Banking

One of Nash’s primary criticisms was directed at the practice of fractional reserve banking. He saw this as a form of legalized fraud, where banks are allowed to lend out more money than they actually have on deposit. Nash argued that this system creates money out of thin air, leading to inflation and economic instability.

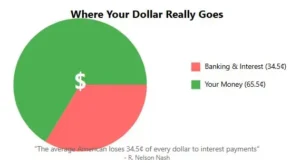

Interest and the Velocity of Money

Nash was particularly concerned with the amount of interest the average person pays over their lifetime. He estimated that the typical American spends around 34.5 cents of every dollar on interest, a figure he found alarming. He believed that by recapturing this interest through the use of whole life insurance policies, individuals could significantly improve their financial situations.

Nash was particularly concerned with the amount of interest the average person pays over their lifetime. He estimated that the typical American spends around 34.5 cents of every dollar on interest, a figure he found alarming. He believed that by recapturing this interest through the use of whole life insurance policies, individuals could significantly improve their financial situations.

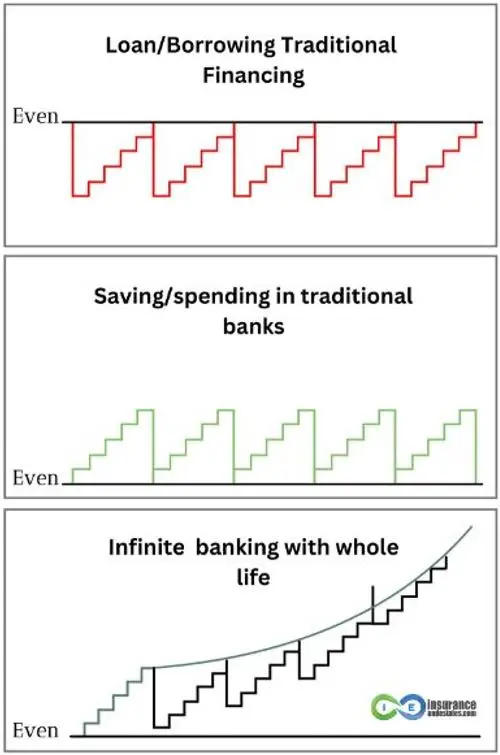

He argued that by becoming your own banker, you could keep your money in motion, continuously cycling it through your policy for personal loans and repayments, rather than letting it sit stagnant or flow to traditional banking institutions. This approach, Nash contended, not only saves on interest payments but also accelerates the growth of wealth by maintaining a high velocity of money within one’s personal economy.

The Illusion of Bank Ownership

Nash challenged the common perception that individuals own the money in their bank accounts. He pointed out that once money is deposited in a bank, it legally becomes the property of the bank. The depositor is merely a creditor of the bank, a situation Nash found problematic.

Government-Sponsored Retirement Plans

Nash was also critical of government-sponsored retirement plans like 401(k)s and IRAs. He saw these as tools used by the government to control people’s money and behavior. He argued that these plans are subject to rule changes at the government’s discretion, making them less reliable than privately owned financial instruments like whole life insurance policies.

The Banking Mindset

Beyond criticizing the banking institutions themselves, Nash also took issue with what he called the “banking mindset” prevalent in society. He believed that people had been conditioned to think like bank customers rather than like bankers. This mindset, he argued, keeps people financially dependent and prevents them from taking full control of their financial lives.

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

The Alternative: Becoming Your Own Banker

As an alternative to the traditional banking system, Nash proposed that individuals should strive to become their own bankers through the use of dividend-paying whole life insurance policies. He believed that by doing so, people could:

As an alternative to the traditional banking system, Nash proposed that individuals should strive to become their own bankers through the use of dividend-paying whole life insurance policies. He believed that by doing so, people could:

- Recapture the interest they would otherwise pay to banks

- Have more control over their money

- Create a stable, predictable financial system for themselves

- Build wealth more efficiently over time through true compound interest growth

- Establish a legacy that could be passed down to future generations

Nash’s critique of the banking system was not just about identifying problems; it was about empowering individuals to take control of their financial lives. Through the Infinite Banking Concept, he offered a practical alternative to what he saw as a flawed and exploitative system.

Key Principles of the Infinite Banking Concept

The Infinite Banking Concept is built on several fundamental principles:

- Everything is financed: Nash emphasized that whether you borrow money or use your own, you’re always financing your purchases through either interest paid or opportunity cost.

- Utilizing dividend-paying whole life insurance as a financial tool: These policies, when properly structured, serve as powerful financial instruments.

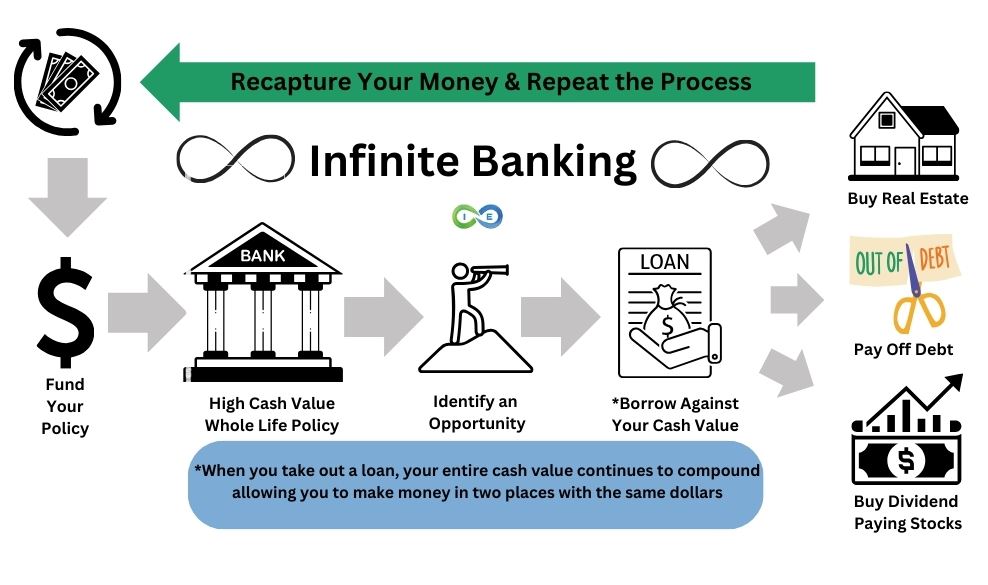

- Becoming your own banker: This involves using the cash value of your life insurance policy as a personal banking system.

- Recapturing the interest typically paid to banks and financial institutions: By borrowing against your policy, you pay interest to yourself rather than to a bank.

- Creating a personal economy that grows independently of external financial systems: This provides financial control and flexibility.

Volume and Scalability

Nelson Nash’s approach was heavily influenced by two key principles: the importance of volume and the scalability of the system.

1. Volume Over Rates:

One of the most revolutionary aspects of Nelson Nash’s Infinite Banking Concept (IBC) is its shift in focus from return on investment to volume of capital flow.

One of the most revolutionary aspects of Nelson Nash’s Infinite Banking Concept (IBC) is its shift in focus from return on investment to volume of capital flow.

Nash emphasized that success in IBC comes from consistently growing your banking system, much like how successful retail businesses focus on volume rather than high profit margins. He believed that the steady accumulation of cash value through regular premium payments and policy loans was more important than chasing high interest rates or returns.

People always talk about return on investment and compare whole life insurance with the stock market, but what Nash is saying is that you put your entire income into a policy so that the volume of your return exceeds what you could ever make in the stock market. Because we’re not talking about rate of return we’re talking about volume.

- Traditional advice: Save 10-15% of income in tax-deferred accounts, focus on ROI.

- Nash’s IBC approach: Funnel entire income through a tax-advantaged whole life insurance policy.

2. Scalability Through Multiple Policies:

To illustrate the scalability of IBC, Nash shared his personal experience of owning 49 life insurance policies at one point. This approach demonstrated that:

- The concept can be expanded to accommodate growing financial needs.

- Multiple policies can be used to create a more robust and flexible banking system.

- The principles of IBC can be applied repeatedly, amplifying its benefits.

Nash’s focus on these aspects underscores the potential of IBC as a long-term wealth-building strategy. By prioritizing volume and demonstrating scalability, he showed how individuals could create a substantial personal banking system over time, continually expanding their financial capacity and control.

Designing an Infinite Banking Policy

Nash provided detailed guidance on structuring a policy for IBC:

1. Dividend Paying Whole Life

Use a dividend-paying whole life policy from a reputable, financially strong insurance company.

2. Mutual Insurance Company

The company should be one of the Top Mutual Insurance Companies versus stocks companies. You can go here to read more about the differences between mutual vs stock insurance companies and why mutual companies are the best choice for infinite banking.

3. Avoid the MEC

Structure the policy to maximize cash value growth while staying within IRS guidelines to avoid creating a Modified Endowment Contract (MEC).

4. PUAs

Utilize a Paid-Up Additions (PUA) rider to increase the policy’s cash value more rapidly.

5. Structure

Aim to get as close to the MEC line as possible without crossing it, reducing the amount of immediate death benefit while emphasizing the banking aspects of the system.

The Infinite Banking Concept: A Grocery Store Analogy

Nash often used the analogy of running a grocery store to explain the Infinite Banking Concept. Here’s how the parallel works:

1. The Grocery Store = Your Whole Life Insurance Policy

– Just as you own a grocery store, you own your insurance policy.

2. Store Inventory (Canned Goods) = Cash Value in Your Policy

– The more inventory you stock, the more you have to sell. Similarly, the more cash value you build, the more you have to “bank” with.

3. Stocking Shelves = Paying Premiums

– Regularly stocking your shelves (paying premiums) ensures you always have inventory (cash value) available.

4. Selling Goods = Taking Policy Loans

– When you need money, you “sell” your inventory by taking a policy loan.

5. Restocking Shelves = Repaying Policy Loans

– Just as you restock shelves after selling goods, you repay policy loans to maintain your “inventory” of cash value.

6. Store Profits = Policy Dividends and Interest

– Your store (policy) generates profits (dividends and interest) which can be reinvested to grow your business.

7. Opening New Branches = Starting Additional Policies

– As your banking system grows, you might open new “branches” (additional policies) to expand your capacity.

8. Front Door vs. Back Door

– Always use the “front door” (pay back loans with interest) rather than the “back door” (defaulting on loans) to maintain the integrity and growth of your system.

9. Volume, Not Rates

– Success comes from consistent, volume-based operations rather than chasing high interest rates.

This analogy illustrates how becoming your own banker through IBC is similar to running a successful business, emphasizing consistent growth, reinvestment, and responsible management.

Nash’s Teaching Methods

Nash developed a unique seminar-based approach to teach IBC. For years before publishing his book, he traveled across the country, delivering in-depth seminars that often lasted several hours. These seminars became the foundation for “Becoming Your Own Banker.”

Nash was known for his engaging Southern charm and his ability to make complex financial concepts accessible to a wide audience. He used simple, relatable examples and a healthy dose of humor to convey his ideas.

The Legacy of Nelson Nash

Nash’s impact on personal finance extended beyond his seminars and book. He established the Nelson Nash Institute (NNI) to ensure the continued spread and evolution of his ideas. Even after Nash’s passing on March 27, 2019, at the age of 88, the IBC movement has continued to grow.

The Infinite Banking Concept in Practice

Implementing IBC involves several key steps:

- Establishing a properly structured, dividend-paying whole life insurance policy

- Nash focused on capitalizing the policy over at least 4-7 years, ideally longer for greater profitability, however, policy can be designed so that 90% of the cash value is available within 30 days.

- Using policy loans to finance purchases or investments

- Repaying the policy loans, effectively paying interest to oneself

- Repeating this process to continually grow one’s personal banking system

Nash suggested that, ultimately, annual life insurance premiums should equal annual income, though this might take 20-25 years to achieve for the average individual.

Addressing Common Concerns and Misconceptions

Nash addressed several common objections to IBC in his work:

- “Whole life insurance is too expensive”: Nash argued that it should be viewed as a strategic asset rather than an expense.

- “I can get a better return elsewhere”: Nash emphasized that IBC is about how you finance purchases, not just about investment returns.

- “It takes too long to build significant cash value”: Nash stressed the long-term nature of wealth building and the ongoing benefits throughout the policy’s life.

The Future of IBC

Today, the Infinite Banking Concept continues to gain traction in the financial world. As traditional financial systems face increasing scrutiny and volatility, many are turning to IBC as a means of creating financial stability and independence.

Nash envisioned IBC as a multigenerational strategy, capable of creating a perpetual banking system that could be passed down to future generations.

Conclusion

R. Nelson Nash’s contributions to personal finance have been truly revolutionary. Through the Infinite Banking Concept, he challenged conventional financial wisdom and offered individuals a path to greater financial control and prosperity.

Nash’s ideas remain profoundly relevant in today’s economic climate. As individuals seek alternatives to traditional banking and investing methods, the principles of IBC offer a compelling solution. By becoming their own bankers, people can take charge of their financial futures, build lasting wealth, and achieve a level of financial independence that might otherwise seem out of reach.

The legacy of Nelson Nash lives on through the countless lives he has impacted and the ongoing growth of the IBC movement. His vision of financial empowerment continues to inspire and guide individuals toward a more secure and prosperous future.

Next Steps

If you’re intrigued by the Infinite Banking Concept and want to explore how it might benefit your financial future, we encourage you to take the next step. Our team of Pro Client Guides is ready to provide personalized consultations tailored to your unique financial situation and goals.

By reaching out, you’ll have the opportunity to:

- Get answers to your specific questions about implementing the concept

- Receive detailed illustrations of how IBC could work for you

- Access ongoing coaching to help you maximize the benefits of IBC

Don’t let this opportunity to transform your financial future pass you by. Contact one of our Pro Client Guides today and start your journey toward becoming your own banker.

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Sources

Becoming Your Own Banker by R. Nelson Nash

The Source of the Source of Nelson Nash’s Infinite Banking Concept, Ryan Griggs