When building your financial plan, there is a wide variety of tools available to you – and because everyone’s goals, risk tolerance, and time frame can differ, some of these may work better than others for you and your specific objectives.

With one of the biggest risks to your financial security being taxes – particularly if (when) income tax rates go up in the future – it is critical to factor in tax reduction and elimination strategies. Two possible options for helping you in this area are the Roth IRA and whole life insurance.

When we say whole life, we mean a properly structured high cash value whole life insurance where the emphasis is on cash value accumulation and growth. This is different from a traditional whole life policy where the emphasis was on the death benefit and the cash value growth was minimal.

Both a Roth IRA and Whole Life Policy can help to reduce your tax burden both before and after you retire. But before you move forward with either of these tax-favored accounts, it is important that you understand how each one works and why one or both of them may (or may not) make sense in your overall financial plan.

Whole Life Insurance versus Roth IRA

| Whole Life Insurance | Roth IRA | |

|---|---|---|

| Pre-tax Contributions | No | No |

| Tax-advantaged Growth | Yes | Yes |

| Guaranteed minimum return | Yes | No |

| Subject to stock market risk | No | Yes |

| Tax-free access to funds | Yes | Yes |

| Death benefit protection | Yes | No |

| Annual maximum contribution limit | No | Yes |

| Required Minimum Distributions (RMDs) | No | No |

| IRS 10% early withdrawal penalty (under age 59 ½) | No | Yes |

| Penalty-free access to funds for healthcare or long-term care needs | Yes | Maybe |

| Time limit on accessing distributions for beneficiaries upon death of the account holder | No | Yes (10 years) |

| Ability to borrow funds | Yes | Limited |

| Continued growth on the full account value - including funds that are "borrowed" | Yes | No |

Planning for Retirement with a Roth IRA

Individual Retirement Accounts (IRAs) are tax-advantaged personal plans that can help you to build up your savings exponentially over time. These accounts can be nice supplements to savings that you may already have in other retirement plans, like an employer-sponsored 401(k) or 403(b).

There are two types of IRAs – traditional and Roth.

With a traditional IRA, you make contributions with pre-tax money. So, you are allowed to take a deduction on your income taxes in the year(s) that you contribute. The money in a traditional IRA account also grows tax deferred, so no taxes are due on the gains until they are withdrawn – which could be at a much later time in the future. This tax deferral can typically outpace fully taxable savings (with all other factors being equal).

Why Tax Deferred is not Always the Best Option

Unfortunately, though, while tax deferral can offer a great way for you to rack up your account value, when the time comes to withdraw your funds, you can lose a significant portion of your money to Uncle Sam – particularly as tax rates are expected to go up in the future.

In fact, over the past century, the top federal income tax rate has been as high as 94% – and there is no guarantee that it won’t go that high again. So, Uncle Sam could end up being the biggest recipient of your savings. This makes tax reduction and elimination strategies essential in your retirement plan.

Top Federal Income Tax Rates in the U.S. 1913 – 2024

| Year | Rate | Year | Rate |

|---|---|---|---|

| 2018-2024 | 37 | 1950 | 84.36 |

| 2013-2017 | 39.6 | 1948-1949 | 82.13 |

| 2003-2012 | 35 | 1946-1947 | 86.45 |

| 2002 | 38.6 | 1944-1945 | 94 |

| 2001 | 39.1 | 1942-1943 | 88 |

| 1993-2000 | 39.6 | 1941 | 81 |

| 1991-1992 | 31 | 1940 | 81.1 |

| 1988-1990 | 28 | 1936-1939 | 79 |

| 1987 | 38.5 | 1932-1935 | 63 |

| 1982-1986 | 50 | 1930-1931 | 25 |

| 1981 | 69.125 | 1929 | 24 |

| 1971-1980 | 70 | 1925-1928 | 25 |

| 1970 | 71.75 | 1924 | 46 |

| 1969 | 77 | 1923 | 43.5 |

| 1968 | 75.25 | 1922 | 58 |

| 1965-1967 | 70 | 1919-1921 | 73 |

| 1964 | 77 | 1918 | 77 |

| 1954-1963 | 91 | 1917 | 67 |

| 1952-1953 | 92 | 1916 | 15 |

| 1951 | 91 | 1913-1915 | 7 |

Items to be mindful of when it comes to traditional IRAs:

✅ Required minimum distributions (RMDs) – You must start withdrawing at least a minimum amount each year from the account starting at age 73 (in 2023). If you do not make these withdrawals – or if you don’t withdraw the full amount that is required – you will incur a penalty from the IRS.

✅ Early withdrawal penalty – If you access money from the account prior to age 59 ½, you will incur an IRS “early withdrawal penalty” of 10%. This is in addition to any taxes that you owe.

✅ 10-year liquidation requirement on inherited IRAs funds – When you pass away, if someone who is not your spouse inherits your IRA, they must fully liquidate the account within ten years – and likewise, pay the corresponding taxes on these withdrawals.

✅ Maximum annual contribution limit – Traditional (and Roth) IRAs cap the amount of money that you can contribute each year. So, given this smaller “foundation” on which to build, it could keep the account value low.

✅ Risk of loss – Depending on what you invest your money in within an IRA account, you could run the risk of loss, both to previous gains and to your original principal.

Pros and Cons of Traditional IRAs

| Traditional IRA Advantages | Traditional IRA Disadvantages |

|---|---|

| Pre-tax contributions | Maximum annual contribution limits |

| Tax deferred growth | Withdrawals are 100% taxable |

| Risk of loss | |

| Early withdrawal penalty | |

| Required minimum distributions (RMDs) |

Roth IRA vs Traditional IRA

While traditional and Roth IRAs share some of the same characteristics, there are also some significant differences between the two.

✅Tax-Free: The earnings and withdrawals in a Roth IRA account are tax-free. This is the case, regardless of income or capital gains tax rates at the time you withdraw the funds.

✅NO RMDs: Also unlike the traditional IRA, there are no mandatory required minimum distributions with Roth IRA accounts at any age. So, it is possible to leave the money in a Roth IRA so it can continue to accumulate on a tax-advantaged basis.

Potential Disadvantages of a ROTH IRA

But even though there are many favorable features that are associated with Roth IRAs, there are still some items to consider, as well.

✅Contribution Limits: For instance, like a traditional IRA, you are only allowed to contribute up to a maximum amount of contribution each year. In this case, if you are age 49 or under in 2023, you may contribute up to $6,500. If you’re age 50 or over, you may add an additional $1,000 in “catch up” contribution, for a total of $7,500. In 2024, these IRA maximum contribution limits go to $7,000 and $8,000 respectively.

✅Total IRA Contributions: Further, if you have both a traditional and a Roth IRA, you are not allowed to contribute the maximum amount each year to both accounts. Rather, your total contribution – regardless of how the funds are divided – may not exceed the total annual dollar amount.

Annual Maximum IRA Contribution

| Age 49 and under | Age 50 and over | |

|---|---|---|

| 2023 | $6,500 | $7,500 |

| 2024 | $7,000 | $8,000 |

✅5 Year Rule: Also, when it comes to taking withdrawals, you are allowed to access your Roth IRA contributions at any time without penalty. However, you may not withdraw the earnings tax free until it has been at least five years since you initially contributed to the Roth account. This is true, regardless of your age at the time you make the withdrawal(s).

✅10% Early Withdrawal Fee: In addition, early distributions (i.e., those that are taken before you reach age 59 ½) will incur a 10% IRS “early withdrawal” penalty.

Pros and Cons of the Roth IRA

| Roth IRA Advantages | Roth IRA Disadvantages |

|---|---|

| Contributions and earnings grow tax-free | No income tax deduction on contributions |

| No required minimum distributions | Maximum income limits to participate |

| Contributions may be withdrawn at any time, tax-free | 10% IRS early withdrawal penalty if earnings are withdrawn before age 59 ½ |

| Tax-free withdrawals | Maximum annual contribution limit |

| Account must have been open - and the initial contribution made - for five years in order to withdraw earnings tax free |

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept

Using Whole Life Insurance for Growth, Protection, and Generating Retirement Income

Although many people only purchase life insurance for the death benefit protection that it offers, a properly designed dividend paying whole life insurance policy can actually provide a long list of added incentives – with most being available while the insured is still alive.

In fact, there are a number of features on a properly structured whole life insurance policy that could deem it as a possible replacement for – or as a supplement to – a Roth IRA.

As with other types of permanent life insurance, whole life insurance offers a death benefit, along with a cash value component.

✅There are several guarantees that are associated with whole life insurance, including the:

- Amount of the death benefit coverage (although the death benefit amount may increase over time based on the policy design)

- Premium amount required

- Minimum return on the growth of the cash value

Whole life insurance coverage will remain in force – even as the insured ages, and if they contract an adverse health condition – provided that the premium is paid.

✅ Tax-Deferred (Potentially Tax-Free) Gains: Similar to with the Roth IRA, whole life insurance cash value is allowed to grow without being taxed on the gains each year. This essentially allows you to generate a return on your principal, as well as on the previous gains, and on the funds that would have otherwise been paid in taxes, providing powerful compound interest growth.

✅ No Contribution Limits Apart from Multiple of Income: Unlike an IRA, your yearly premium payments aren’t “capped” at just $7,000 or $8,000. Your initial contribution limit is typically capped at a multiple of income (MOI), based on your age. So, given the tax-advantaged growth that whole life offers – in addition to no having annual maximum contribution limits apart from the MOI – it could be a great outlet for adding to your tax-favored savings, even if you have already “maxed out” the annual contributions to an IRA and/or employer-sponsored retirement plan.

✅ Annual Dividends: Further, depending on where you purchase your whole life insurance policy, you may also be eligible for life insurance dividend payments. Because dividends are considered a return of excess premium by the IRS, they are received tax free – and as such, they can be added to the cash value in your policy to add to the overall growth.

Although dividend payments are not guaranteed, some of the top, highly rated mutual life insurance companies have been making regular dividend payments to their policyholders for more than 100 years.

But that’s just the beginning of the benefits that can be offered through a whole life insurance policy.

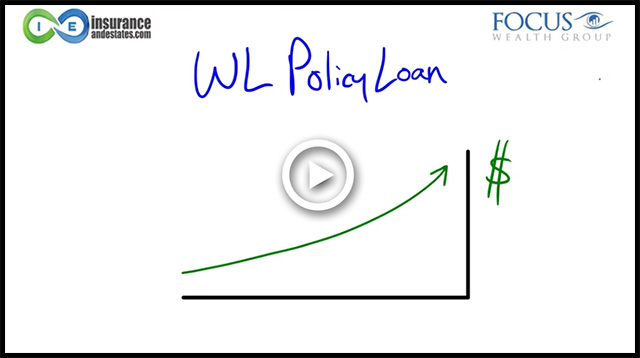

✅ Tax Free Policy Loans: You are also allowed to access the policy’s cash value, either via withdrawals or loans, for any reason. Any part of a withdrawal that is considered gain is taxable (above your basis, or premiums paid into the policy). But, if you instead take a policy loan, you can access the funds tax free.

Using Whole Life Policy Loans Examples

Although most people don’t necessarily want to take on more “debt,” life insurance policy loans work differently than more “traditional” loans from banks or other lenders.

For instance, there is no credit or income check needed to qualify for the life insurance loan. Rather, you simply contact the insurance company and let them know how much you need, and you will typically have the funds available to you within days.

Also, life insurance policy loans do not show up on your credit report. Therefore, they won’t reduce your credit score or hinder you from obtaining other types of financing that you may be applying for.

✅ Become Your Own Banker: Those who own properly structured whole life insurance policies can even “become their own banker,” because they are able to use their cash value to easily make purchases like vehicles, business equipment, and real estate – and then pay themselves back and repeat the process again.

✅ Possible Wash Loan: While the insurance company will generally charge interest on the loan, it could turn out to be a “wash” – or possibly still profitable to you – if the return on the cash value is higher than the interest that is charged on the loan. This is known as arbitrage. So, you could essentially borrow money and be “paid” to do so.

✅ Cash Value Compound Interest Growth: One of the best features of a whole life insurance policy loan is that the entire amount of your cash value will continue to generate interest. So, for instance, if your policy has a cash value of $100,000 and you borrow $40,000 against it, you will continue to get interest on the whole $100,000 in your cash value account. This is because you are actually borrowing from the insurance company and simply using your cash value as collateral.

✅ No Requirement to Repay Loan: While it is recommended that you make payments towards repaying your life insurance policy loan, if the full balance is not repaid at the time the insured passes away, the remainder will be paid using proceeds from the death benefit – and then any of the remaining death benefit funds will be paid out (income tax free) to the beneficiary(ies).

✅ Living Benefits: Many whole life insurance policies also offer “living benefits.” This refers to penalty-free access to funds for situations like:

- Terminal, chronic, and/or critical illness diagnosis

- Need for long-term care services

✅ Leveraged Death Benefit: You can have all of these benefits from a whole life insurance policy, while at the same time also having a financial safety net (i.e., the death benefit) in place for your loved ones – money that is received income tax free by your beneficiaries, and without any time limit imposed on when they must access the funds.

Possible Disadvantages of Whole Life Insurance

Even so, there are some considerations to keep in mind when obtaining a whole life insurance policy.

✅Must Qualify: One potential disadvantage is the underwriting that is required to qualify for the policy. Therefore, the insured should be in relatively good health at the time of application.

✅MEC Limits: In addition, it is important to keep the policy within certain guidelines so it does not become a “Modified Endowment Contract” (MEC) and lose its tax-related benefits. A Modified Endowment Contract is a type of tax qualification for a life insurance policy where its cumulative premiums exceed the federal tax law limits. If this happens, the taxation structure, along with the policy’s classification, changes.

Working with qualified whole life insurance specialist can help you to ensure that your policy remains within the proper guidelines, while at the same time maximizes the growth of the cash value.

Pros and Cons of Whole Life Insurance

| Whole Life Insurance Advantages | Whole Life Insurance Disadvantages |

|---|---|

| No maximum annual contribution limit | Must qualify for coverage through underwriting |

| No required minimum distributions | Must ensure that the policy does not become a Modified Endowment Contract (MEC) |

| Tax-advantaged growth | |

| Guaranteed minimum return | |

| Premium will not increase (even as the insured ages) | |

| May receive dividends (tax-free) | |

| No stock market risk | |

| Death benefit protection | |

| Funds available for "living benefits" like illness and long-term care needs | |

| Return continues being paid on "borrowed" funds | |

| Easy and fast access to funds for high-ticket purchases |

Which is Better – Roth IRA or Whole Life Insurance?

With all of the benefits that are available via Roth IRAs and whole life insurance, which financial vehicle is better for you? There is a good chance that the answer to the question will be…Both.

Because not all situations are the same, the tools that are used to accomplish certain goals can differ. In any case, though, when determining which of these tax-advantaged tools is right for you, there are some important factors to keep in mind, such as:

✅Other tax-favored savings you have (such as qualified retirement plans)

✅Other taxable and tax-free income generators

✅Current and future (anticipated) income tax bracket

✅Need for death benefit protection

✅Legacy plans

✅Anticipated life expectancy

✅Current (and anticipated future) health condition

✅Other funds available for possible uninsured healthcare and/or long-term care needs

Should Whole Life Insurance Be Part of Your Financial Plan?

Your financial, retirement, and estate plan can revolve around numerous short- and long-term objectives. With that in mind, it is critical that you have the right tools in place to help you achieve those goals. A whole life insurance policy could be a viable option for you.

But, because not all whole life insurance policies – and the insurers that offer them – are exactly the same, it is best if you first discuss your specific situation with an experienced life insurance specialist who can guide you in the right direction.

So, if you’re ready to learn more about how you can build up your savings and generate an ongoing and reliable tax-free cash flow – regardless of what happens in the stock market – contact us today and talk with one of our Pro Client Guides. You can reach us by calling (877) 787-7558 or send us an email at info@insuranceandestates.com. We look forward to hearing from you.

THE ULTIMATE FREE DOWNLOAD

The Self Banking Blueprint

A Modern Approach To The Infinite Banking Concept