Licensed Practitioner Responds to Dave’s Whole Life Claims

By Barry Brooksby, Authorized Nelson Nash Infinite Banking Practitioner & Real Estate Strategist

With over 25 years of experience helping clients take control of their wealth, Barry has guided families through large-scale real estate investing, traditional financial services, and advanced infinite banking strategies. As an Authorized Nelson Nash Infinite Banking Practitioner and creator of the Amazing Life Agent program, Barry specializes in designing high cash value whole life policies that maximize client outcomes over commission structures.

📋 Key Takeaway for Dave Ramsey Graduates

Dave Ramsey’s debt elimination advice saved your financial life. Now it’s time to graduate to wealth-building strategies that wealthy families actually use. While Dave teaches Baby Steps that work for people drowning in debt, high cash value whole life insurance offers advanced tools for those ready to move beyond financial survival to generational wealth building.

📊 Quick Facts: Why This Matters for Graduates

| Dave’s Target Audience: | People drowning in debt needing basic financial discipline |

| Your Current Status: | Debt-free graduate ready for advanced wealth strategies |

| Banks Hold in “Scam” Insurance: | $180+ billion in Bank-Owned Life Insurance (BOLI) |

| High Cash Value Policy Returns: | 5%+ guaranteed tax-free vs. Dave’s 12% mythology |

| Commission Structure: | 70-90% LOWER than traditional whole life policies |

🎥 Watch: REACTION – Dave Ramsey is Wrong About High Cash Value Whole Life Insurance

See the mathematical breakdown that proves Dave’s whole life criticism is flawed. We analyze his claims with real policy data and show how properly structured whole life actually supports his core financial principles.

Can’t watch now? Continue reading below for the complete written analysis with additional policy illustrations and expert insights.

Table of Contents

- Graduation Time: Moving Beyond Financial Survival

- What Wealthy Families Actually Do

- General Concept and Policy Design

- Cash Value and Dividend Reality

- Policy Loans and True Flexibility

- Death Benefit Facts vs. Fiction

- Cost and Value: The Real Comparison

- Investment Comparisons: Math vs. Marketing

- Real Estate and Business Applications

- Financial Advisors and Agent Motivations

- Conclusion: Your Graduate-Level Decision

- Frequently Asked Questions

🔗 Part of Our Dave Ramsey Analysis Series: This expert response builds on our comprehensive review of Dave Ramsey’s financial advice. For the complete analysis including mathematical proof of his flawed assumptions and business model conflicts, explore our full research series.

Graduation Time: Moving Beyond Financial Survival

Congratulations! If you’re reading this, you’ve likely completed Dave Ramsey’s Baby Steps and escaped the debt trap that enslaves millions of Americans. Dave’s advice works brilliantly for people drowning in financial chaos who need simple, actionable steps to regain control.

But here’s what Dave won’t tell you: his advice is designed for financial kindergarten, not graduate school. As we detailed in our comprehensive Dave Ramsey analysis, his advice works for financial survival but limits wealth-building potential for graduates ready for advanced strategies.

Dave built his media empire by getting into churches and selling simple sound bites to well-meaning families desperate for financial rescue. His debt elimination principles provide solid foundation work – pay off debt, build emergency funds, live below your means. These fundamentals never change and remain valuable throughout your wealth-building journey.

However, once you’ve mastered financial basics and are ready for Baby Step 7 (building wealth and giving), you need sophisticated strategies that wealthy families actually use, not oversimplified radio advice designed for mass audiences still struggling with credit card debt.

💡 Key Insight: The Graduation Principle

Dave teaches financial survival skills. Once you’re debt-free with emergency funds, you need financial prosperity strategies. That’s the difference between remedial education and advanced wealth building.

What Wealthy Families Actually Do With Life Insurance

Before examining Dave’s specific claims about whole life insurance, let’s examine how affluent families and sophisticated institutions actually use these tools:

The $180 Billion Banking Secret

Banks hold over $180 billion in Bank-Owned Life Insurance (BOLI) according to the Federal Deposit Insurance Corporation. If whole life insurance is such a terrible financial vehicle, why do the most regulated and scrutinized financial institutions in America hold massive positions in it?

| Institution Type | Why They Use Whole Life Insurance |

| Banks | Guaranteed returns, tax advantages, regulatory capital benefits |

| Corporations | Tax-efficient employee benefit funding, key person protection |

| Wealthy Families | Estate planning, tax-free wealth transfer, infinite banking strategies |

| Financial Institutions | Stable balance sheet assets, predictable returns |

This institutional usage directly contradicts Dave’s claims, as we explored in our mathematical comparison of guaranteed returns vs volatile markets. The question that challenges Dave’s absolute statements: If these institutions employ armies of CFAs, actuaries, and financial analysts, why would they choose “scam” insurance products for their own balance sheets?

Modern High Cash Value Design vs. “Old School” Policies

Dave’s criticism of whole life insurance demonstrates a fundamental misunderstanding of modern policy design. When he calls infinite banking policies “old school done poorly,” he reveals ignorance about how these products have evolved.

Here’s what Dave doesn’t understand about high cash value whole life policies designed for infinite banking:

Addressing Dave’s Claims: General Concept and Policy Design

Claim #1: “IBC and whole life insurance are scams”

Graduate-Level Analysis: This characterization reveals either deliberate misrepresentation or fundamental ignorance about regulated insurance products. Whole life insurance is governed by state insurance commissioners with strict reserve requirements, regulatory oversight, and consumer protections.

The Infinite Banking Concept isn’t a product – it’s a strategy for using these regulated financial tools. Major corporations like Walmart, General Electric, and Bank of America hold billions in cash value life insurance precisely because of the legitimate benefits Dave claims don’t exist.

Calling regulated insurance products “scams” while promoting volatile mutual fund investments through referral fee arrangements raises questions about whose financial interests are really being served.

Claim #2: “Whole life insurance is old school done poorly”

What Wealthy Families Know: Modern high cash value whole life policies designed for infinite banking are fundamentally different from traditional whole life policies your grandfather might have owned.

| Traditional Whole Life (What Dave Criticizes) | High Cash Value Design (What Graduates Use) |

| Maximizes death benefit | Maximizes cash value accumulation |

| High agent commissions | 70-90% lower commission structure |

| Limited premium flexibility | Flexible premium payments (minimum to maximum) |

| Slow cash value growth | Accelerated cash value through paid-up additions |

| Insurance-focused | Banking and wealth-building focused |

Dave’s “old school” criticism demonstrates that he’s either unaware of modern policy designs or deliberately misrepresenting them to protect his referral revenue streams from investment companies.

Claim #3: “Infinite Banking policies are just traditional whole life policies”

Advanced Perspective: This claim reveals Dave’s complete misunderstanding of specialized policy architecture. High cash value whole life policies designed for infinite banking incorporate sophisticated features that traditional policies lack:

- Paid-Up Additions Riders: PUAs accelerate cash value growth by purchasing additional insurance with guaranteed returns

- Term Blending: Optimize the death benefit-to-premium ratio for maximum cash accumulation

- Flexible Premium Structure: Pay anywhere from minimum required to maximum allowed based on financial goals

- Banking-Focused Design: Emphasize policy loan capabilities and cash flow optimization

- Reduced Commission Impact: Structure results in dramatically lower agent compensation, aligning interests with clients

💡 Graduate Insight: Commission Reality

High cash value policies designed for infinite banking typically generate 70-90% lower commissions than traditional whole life insurance. Agents who recommend these products are often sacrificing income to provide better client outcomes – the opposite of Dave’s “greedy agent” narrative.

Cash Value and Dividend Reality

Claim #4: “Cash value in whole life policies dies with you”

Mathematical Truth for Graduates: This claim demonstrates fundamental misunderstanding of how life insurance death benefits work. Cash value doesn’t “die with you” – it’s part of the death benefit paid to your beneficiaries.

Here’s what Dave gets wrong: In a whole life policy, cash value represents the present value of the future death benefit. When you die, beneficiaries receive the full death benefit, which includes the accumulated cash value.

Real Policy Illustration: Death Benefit Growth

Actual high cash value policy for 31-year-old with $25,000 annual premium:

| Year | Age | Cash Value | Total Death Benefit | Benefit Growth |

| 1 | 31 | $18,673 | $729,145 | Base amount |

| 5 | 35 | $110,565 | $1,039,697 | +$310,552 |

| 10 | 40 | $244,807 | $1,435,812 | +$706,667 |

| 15 | 45 | $395,732 | $1,851,746 | +$1,122,601 |

| 20 | 50 | $564,986 | $2,292,901 | +$1,563,756 |

Key Point: The death benefit grows from $729,145 to over $2.2 million by year 20 – a 314% increase. Dave’s claim that “only the face value is paid out” is mathematically false for properly designed policies.

Claim #5: “Dividends are just a return of overcharged premiums”

What Sophisticated Investors Understand: While dividends from mutual insurance companies do include some premium return component, they primarily reflect the company’s investment performance, mortality experience, and operational efficiency.

Mutual insurance companies invest policyholder premiums in high-grade bonds, real estate, and other assets. When these investments perform well, profits are shared with policyholders through dividends. The top mutual companies Dave criticizes have paid dividends for over 100 consecutive years, including through the Great Depression, multiple recessions, and market crashes.

| Dividend Components | What It Means |

| Investment Returns | Profits from bond portfolios, real estate, and other investments |

| Mortality Experience | When fewer people die than expected, savings passed to policyholders |

| Operational Efficiency | When companies operate more efficiently than projected |

| Premium Adjustments | Small portion reflecting conservative premium pricing |

Claim #6: “Cash values in policies are just sitting there”

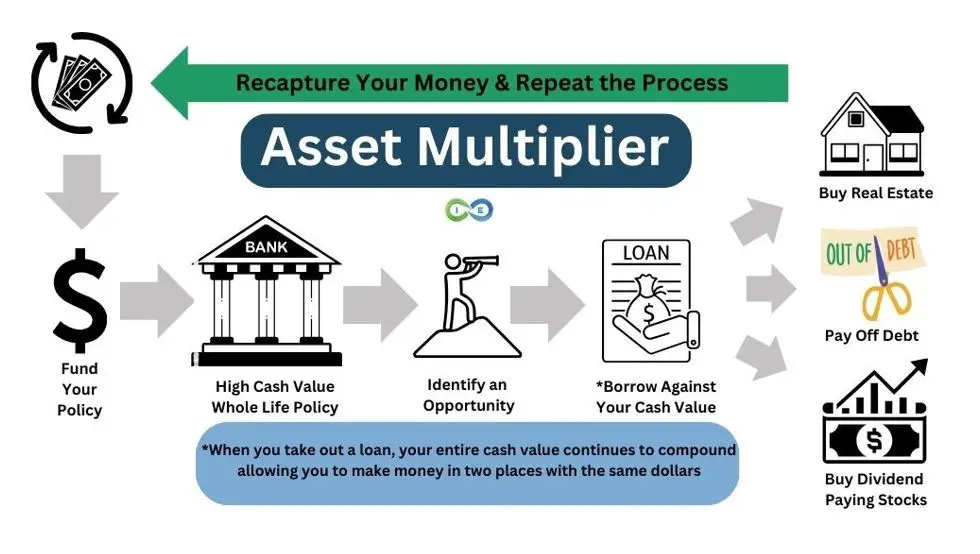

Advanced Financial Strategy: This reveals Dave’s complete ignorance of how infinite banking practitioners use cash value. In a properly designed high cash value policy, money is never “sitting there” – it’s actively deployed for maximum financial leverage through the Asset Multiplier strategy.

Here’s how sophisticated wealth builders use policy cash value:

- Guaranteed Growth: Cash value earns 4-6% guaranteed plus potential dividends

- Strategic Deployment: Policy loans provide capital for real estate, business investments, or market opportunities

- Opportunity Maximization: Deploy cash during market crashes while full cash value continues growing

- Tax Optimization: Access growth tax-free through policy loans rather than taxable withdrawals

- Banking Replacement: Eliminate dependence on traditional banks and their approval processes

The Asset Multiplier Blueprint: Your cash value continues earning while you deploy policy loans for investments

💡 Infinite Banking in Action

Real Example: Take a $100,000 policy loan for real estate down payment. Your $200,000 cash value continues earning 5% on the full amount while your rental property generates additional returns. You’re earning returns on both the deployment AND the policy growth simultaneously – making money in two places with the same dollars.

🔄 The Asset Multiplier Process

- Fund Your Policy: Build substantial cash value through consistent premiums

- Identify Opportunities: Real estate, business investments, or market crashes

- Deploy Capital: Take policy loans while cash value keeps growing

- Generate Returns: Earn from both your investment AND continued policy growth

- Recapture & Repeat: Pay back loans and repeat the process with even more capital

This creates true infinite banking – your own financial ecosystem that compounds wealth regardless of external market conditions.

📝 Section Summary: Cash Value and Dividend Reality

Key Graduate Insights: Cash value doesn’t “die with you” – real policy data shows 314% death benefit growth over 20 years from $729,145 to $2,292,901. Dividends reflect company investment performance, not just premium returns. Through the Asset Multiplier strategy, cash value is never “sitting there” but actively deployed for real estate and investments while continuing to earn guaranteed returns in the policy.

Policy Loans and True Financial Flexibility

Claim #7: “Borrowing against policies means borrowing your own money”

Graduate-Level Understanding: This demonstrates Dave’s fundamental misunderstanding of how life insurance loans work. You’re not borrowing your own money – you’re borrowing from the insurance company using your cash value as collateral.

Here’s the sophisticated advantage Dave misses:

| Policy Loan Mechanics | Why This Creates Leverage |

| Insurance company loans you money | Your cash value stays in policy, continuing to grow |

| Cash value serves as collateral | No credit checks, qualification, or approval process |

| You control loan repayment terms | Flexible repayment without monthly payment requirements |

| Loan isn’t taxable income | Access capital without tax consequences |

The key advantage: Your cash value continues earning returns on the full amount while you deploy borrowed capital for additional investments. This creates leverage that traditional banking relationships can’t match.

Claim #8: “Whole life insurance isn’t flexible enough for changing financial needs”

Advanced Flexibility Features: Modern high cash value whole life policies offer sophisticated flexibility that Dave either doesn’t understand or deliberately ignores:

Premium Flexibility

- Minimum Premium: Pay the base amount required to keep policy in force

- Target Premium: Optimal payment for planned cash value growth

- Maximum Premium: Highest allowable payment under IRS guidelines for maximum accumulation

- Variable Payments: Adjust premiums based on cash flow or financial priorities

Access Flexibility

- Policy Loans: Access up to 90% of cash value without penalties

- Partial Withdrawals: Remove basis without loan interest in some policies

- Paid-Up Additions: Purchase additional insurance with excess cash

- Dividend Options: Choose how to deploy annual dividends for optimal growth

📝 Section Summary: Policy Loans and True Flexibility

Key Graduate Insights: Policy loans aren’t “borrowing your own money” – you’re borrowing from the insurance company while your cash value continues growing uninterrupted. Modern high cash value policies offer sophisticated flexibility: variable premium payments (minimum to maximum), access to 90% of cash value without penalties, and no credit qualification requirements. This creates banking capabilities that traditional financial institutions can’t match.

Death Benefit: Facts vs. Dave’s Fiction

Claim #9: “Only the face value of the policy is paid out at death”

What Wealthy Families Know: This is completely incorrect for high cash value whole life policies designed for infinite banking. The death benefit grows significantly over time due to paid-up additions and the policy’s structure.

Real Policy Illustration: Death Benefit Growth

Actual high cash value policy for 31-year-old with $25,000 annual premium:

| Year | Age | Cash Value | Total Death Benefit | Benefit Growth |

| 1 | 31 | $18,673 | $729,145 | Base amount |

| 5 | 35 | $110,565 | $1,039,697 | +$310,552 (43% increase) |

| 10 | 40 | $244,807 | $1,435,812 | +$706,667 (97% increase) |

| 15 | 45 | $395,732 | $1,851,746 | +$1,122,601 (154% increase) |

| 20 | 50 | $564,986 | $2,292,901 | +$1,563,756 (214% increase) |

Mathematical Reality: Dave’s claim that “only the face value is paid out” is demonstrably false. This policy’s death benefit grows 214% over 20 years, from $729,145 to $2,292,901.

Compare this to Dave’s “buy term and invest the difference”: Term coverage expires or becomes unaffordable exactly when death probability increases most, leaving families unprotected when they need it most.

💰 The Immediate Leverage Advantage

Day One Protection: This 31-year-old immediately has $729,145 in death benefit protection – nearly 30X leverage on their first $25,000 premium. Dave’s “invest the difference” strategy provides zero death benefit leverage and depends on decades of market cooperation to potentially reach similar wealth levels.

The psychological benefit Dave ignores: A growing death benefit provides peace of mind knowing your family’s financial security improves over time, regardless of market conditions or personal health changes. This certainty allows families to take strategic risks in other areas, knowing their foundation is permanently protected.

Cost and Value: The Real Comparison

Claim #10: “Whole life insurance is too expensive compared to term insurance”

Sophisticated Cost Analysis: This comparison reveals Dave’s oversimplified thinking about financial tools. Comparing whole life to term insurance is like comparing a house purchase to apartment rent. They serve different purposes and time horizons.

| Comparison Factor | Term Insurance | High Cash Value Whole Life |

| Initial Cost | Lower | Higher |

| Long-term Cost | Increasing premiums, eventual expiration | Level premiums, permanent coverage |

| Cash Value | Zero | Guaranteed growth plus dividends |

| Banking Capability | None | Full banking replacement |

| Tax Advantages | None | Tax-free growth, loans, and death benefit |

| Retirement Income | None | Tax-free retirement income via policy loans |

High cash value whole life policies often include term insurance components in early years, giving you both permanent coverage AND temporary additional protection during wealth-building years.

Claim #11: “Buy term and invest the difference is always better”

Real-World Graduate Analysis: Buy Term and Invest the Difference, a/k/a BTID, is an oversimplified strategy ignores several critical factors that sophisticated wealth builders understand:

The Human Factor Dave Ignores:

- Discipline Failure: Most people don’t consistently “invest the difference” over 20-30 years

- Market Timing: Panic selling during crashes destroys long-term returns

- Tax Reality: Investment gains face annual taxation reducing compound growth

- Sequence Risk: Market crashes early in retirement devastate withdrawal-based strategies

The Term Insurance Problem:

- Increasing Premiums: Term costs explode as you age

- Health Changes: Medical issues make renewal impossible

- Coverage Gaps: Most term policies expire when death risk is highest

- No Banking: Zero financial flexibility for opportunities

⚠️ The Term Insurance Trap

A 45-year-old’s 20-year term policy expires at 65 – exactly when death probability increases dramatically. Renewal at 65 typically costs 10-20x the original premium, making coverage unaffordable when you need it most.

💡 The Zander Partnership Smoking Gun

Here’s the ultimate business model contradiction: Zander Insurance literally cannot offer whole life insurance – they only sell term products by design. Dave’s “whole life is a scam” isn’t financial advice, it’s protecting his advertising partner’s limited business model.

When Dave attacks whole life insurance while directing followers to Zander, he’s not recommending the “best” insurance solution, he’s recommending the only solution his referral partner can provide. This isn’t advice; it’s revenue protection disguised as financial education.

This business model conflict is part of broader concerns we identified in our consumer analysis of Dave’s revenue streams.

Key Question: How can Dave claim to offer objective insurance advice when his endorsed partner is contractually prohibited from offering half the available insurance options?

Investment Comparisons: Math vs. Marketing

Claim #12: “Whole life insurance is a poor investment compared to mutual funds”

Graduate-Level Investment Analysis: This comparison reveals Dave’s fundamental misunderstanding of financial tools and their purposes. Whole life insurance isn’t trying to be a mutual fund, it’s providing guarantees, tax advantages, and capabilities that mutual funds can’t deliver.

| Feature | Mutual Funds | High Cash Value Whole Life |

| Return Potential | Higher potential, with market risk | Lower but guaranteed + dividends |

| Market Risk | Full exposure to volatility | Zero market risk |

| Tax Treatment | Annual taxation on gains | Tax-free growth and access |

| Death Benefit | Account value only | Immediate leverage, permanent protection |

| Creditor Protection | Limited or none | Strong asset protection in most states |

| Banking Capability | Must liquidate for access | Policy loans without interrupting growth |

Sophisticated investors don’t choose between mutual funds OR whole life insurance – they use both tools for different purposes in a comprehensive wealth strategy.

Claim #13: “Investing in mutual funds would yield much higher returns (12% annual returns)”

Mathematical Reality Check: Dave’s 11-12% return assumptions have been debunked by leading academic researchers and are based on misleading arithmetic averages rather than actual geometric returns. For example, leading financial researchers David Blanchett (Head of Retirement Research at PGIM) and Michael Finke have publicly refuted Dave’s mathematical assumptions, calling 12% expectations “absolutely nuts” and pointing out his fundamental errors in understanding returns, which Dave to this day refuses to acknowledge.

🚨 The 12% Return Myth Exposed

Dave’s Promise vs. Mathematical Reality (2000-2024):

- Dave’s 12% Promise: $100,000 becomes $1,700,006

- Actual S&P 500 Performance: $100,000 becomes $531,808

- Shortfall: $1,168,198 less than promised

- Actual Geometric Return: 6.91% annually

Volatility stole $231,572 from investors through the difference between arithmetic and geometric means – mathematical reality Dave refuses to acknowledge. For complete mathematical proof of this shortfall, see our detailed analysis of Dave Ramsey’s 12% mythology vs 5% reality.

⚖️ The Licensing and Accountability Gap

Dave promises 12% returns despite irrefutable evidence to the contrary. However, he operates without the licenses or fiduciary responsibilities that govern actual financial professionals:

| Dave Ramsey | Licensed Financial Advisors |

| No securities licenses | Series 7, 66, state licenses required |

| No fiduciary responsibility | Legal obligation to act in client’s best interest |

| Can make unrealistic projections | Prohibited from misleading return assumptions |

| No regulatory oversight | FINRA, SEC, and state regulation |

| Media personality protection | Professional liability and compliance requirements |

Key Point: If a licensed financial advisor made Dave’s 12% return claims or recommended his 8% withdrawal rates, they could face regulatory sanctions, fines, or license revocation. Dave operates in the entertainment/media space without these professional constraints or accountability measures.

For more, see our our article on Dave’s 12% Mythology vs 5% Reality.

Claim #14: “The returns on whole life insurance are too low to be worthwhile”

Sophisticated Return Analysis: This narrow focus on single-metric returns ignores the multifaceted value proposition that sophisticated wealth builders understand:

Total Return Components in High Cash Value Whole Life:

- Guaranteed Base Return: 3-4% contractually guaranteed

- Dividend Participation: Additional 1-2% returns from company performance

- Tax Advantages: Tax-free growth equivalent to higher taxable returns

- Death Benefit Leverage: Immediate wealth multiplication

- Banking Velocity: Ability to earn returns on deployed capital while policy continues growing

- Opportunity Enhancement: Capital available during market crashes for strategic deployment

💡 The Total Return Reality

A tax-free 5% return often equals 7-8% taxable return for high earners. Add banking capabilities, death benefit leverage, and strategic deployment opportunities, and the total value proposition often exceeds volatile market strategies with dramatically less stress.

📝 Section Summary: Investment Comparisons – Math vs. Marketing

Key Graduate Insights: Dave’s 12% return promises delivered only 6.91% actual returns (2000-2024), creating a $1,168,198 shortfall on $100K invested. Unlike licensed financial advisors who face regulatory sanctions for such claims, Dave operates without securities licenses or fiduciary responsibility. High cash value whole life provides multifaceted value: guaranteed 5% tax-free returns, death benefit leverage, banking capabilities, and strategic deployment opportunities that volatile markets can’t match.

Real Estate and Business Applications

Claim #15: “Using whole life insurance for real estate investing is not effective”

Advanced Real Estate Strategy: This claim demonstrates Dave’s ignorance of how sophisticated real estate investors actually finance deals. Infinite banking practitioners have successfully used policy loans for real estate investments for decades.

Policy Loan Advantages for Real Estate:

- No Credit Qualification: Access capital without credit checks or debt-to-income ratios

- Flexible Terms: You control repayment schedule, not a bank

- Continued Growth: Policy cash value keeps earning while you deploy loan proceeds

- Tax Benefits: Policy loans aren’t taxable income

- Speed: Access capital within 30 days, not 30-60 days for traditional financing

- Privacy: No financial disclosure or approval committees

Real-World Example:

Year 10 of high cash value policy with $200,000 cash value:

- Take $150,000 policy loan for real estate down payment

- Purchase $500,000 rental property generating $3,500/month cash flow

- Use rental income to repay policy loan over 5-7 years

- Policy cash value continues earning on full $200,000 during repayment

- End result: Own the property + larger cash value base + death benefit protection

Claim #16: “Major corporations and banks don’t see value in whole life insurance”

Institutional Reality: This claim is factually incorrect and easily disproven by examining corporate balance sheets and regulatory filings.

| Institution Type | Usage | Dollar Amount |

| U.S. Banks | Bank-Owned Life Insurance (BOLI) | $180+ billion |

| Walmart | Corporate-Owned Life Insurance | $4+ billion |

| General Electric | Employee benefit funding | $2+ billion |

| Wells Fargo | Balance sheet optimization | $18+ billion |

The question challenging Dave’s expertise: If whole life insurance provides such poor value, why do the most sophisticated financial institutions in America hold hundreds of billions in these “terrible” investments?

📝 Section Summary: Real Estate and Business Applications

Key Graduate Insights: Policy loans provide superior real estate financing: no credit checks, flexible repayment terms, 30-day access, and continued policy growth during deployment. Dave’s claim that institutions don’t use whole life is factually wrong – U.S. banks hold $180+ billion in BOLI, Walmart holds $4+ billion, and Wells Fargo holds $18+ billion. These sophisticated institutions choose whole life for guaranteed returns, tax advantages, and balance sheet optimization that Dave claims don’t exist.

Financial Advisors and Agent Motivations

Claim #18: “Financial advisors recommending whole life are not acting in clients’ best interests”

Professional Reality Analysis: This broad generalization ignores several important factors about modern high cash value policy design and professional motivations:

Commission Structure Reality:

- Reduced Commissions: High cash value policies designed for infinite banking typically pay 70-90% lower commissions than traditional whole life

- Client Focus: Advisors specializing in these strategies often sacrifice income for better client outcomes

- Long-term Relationships: Success depends on client satisfaction and referrals, not product sales

- Fiduciary Standards: Many advisors have legal obligations to act in clients’ best interests

The Asset Management Conflict Dave Ignores:

Traditional financial advisors often avoid recommending life insurance because it reduces assets under management (AUM), directly impacting their recurring revenue. Dave’s SmartVestor Pro network collects ongoing fees from managed assets, a direct conflict when considering strategies that don’t generate management fees.

💡 The Real Conflict of Interest

Dave attacks insurance professionals for earning commissions while collecting referral fees from SmartVestor Pro advisors and Zander Insurance partnerships. His business model generates revenue regardless of follower investment performance – a structure that continues profiting even when advice fails.

Claim #19: “Insurance agents only recommend whole life because they make big commissions”

Graduate-Level Professional Analysis: This outdated stereotype ignores modern policy design and professional practices:

Modern High Cash Value Policy Economics:

- Commission Reduction: 70-90% lower than traditional whole life policies

- Client Optimization: Designed to maximize client cash value, not agent compensation

- Professional Standards: Many agents undergo specialized infinite banking training

- Long-term Focus: Success measured by client outcomes, not initial sales

Comparative Commission Analysis:

| Product Type | Typical Commission | Ongoing Revenue |

| Traditional Whole Life | 90-110% of first year premium | Renewal commissions for years |

| High Cash Value IBC Design | 10-30% of first year premium | Minimal renewal commissions |

| Mutual Fund Sales | 3-6% upfront commission | 1-2% annual management fees |

Agents recommending high cash value designs often earn less initially but focus on long-term client relationships and referrals based on actual results.

Conclusion: Your Graduate-Level Decision

Dave Ramsey’s debt elimination principles provided your financial foundation, and that foundation remains valuable throughout your wealth-building journey. His emphasis on living below your means, avoiding consumer debt, and building emergency funds creates the stability necessary for advanced strategies.

But once you’ve mastered financial basics and are ready for sophisticated wealth building, you need tools that wealthy families actually use, not oversimplified advice designed for mass audiences still struggling with credit card payments.

The Graduate Decision Framework:

| Financial Stage | Appropriate Strategy | Focus |

| Drowning in Debt | Dave Ramsey Baby Steps 1-6 | Financial survival and debt elimination |

| Debt-Free Graduate | High cash value whole life + advanced strategies | Wealth building and generational planning |

| Established Wealth | Infinite banking ecosystem | Multi-generational wealth transfer |

The Key Questions for Graduates:

- Do you want guaranteed growth with tax advantages, or volatile returns with tax consequences?

- Do you prefer permanent death benefit protection, or temporary coverage that expires when you need it most?

- Would you rather be your own banker, or depend on traditional institutions for approval?

- Do you want financial strategies that create peace of mind, or anxiety about market performance?

Your financial education journey continues beyond Dave’s baby steps. The choice isn’t between having money or not having money, it’s between two different approaches to building and preserving wealth for generations.

Wealthy families don’t follow conventional advice from media personalities with business model conflicts. They create their own financial ecosystems using strategies like infinite banking that provide certainty, control, and generational wealth transfer capabilities.

📚 Continue Your Dave Ramsey Graduate Education

Our comprehensive investigation examines Dave Ramsey’s financial advice from multiple angles:

Core Analysis & Mathematical Proof

Expert Insurance Analysis

Discover if High Cash Value Whole Life Insurance is Right for You

Before committing to this advanced wealth-building strategy, get a personalized analysis from our independent advisory team. We’ll help you understand if high cash value whole life insurance truly aligns with your financial goals and wealth-building objectives.

- ✓ Receive a detailed breakdown of how high cash value whole life would work in your specific situation

- ✓ Compare infinite banking to conventional investment strategies and Dave Ramsey’s approach

- ✓ Understand the potential tax advantages and death benefit leverage benefits

- ✓ Get a clear explanation of all features and implementation requirements

Schedule your complimentary 30-minute high cash value whole life analysis today and take the first step toward becoming your own banker.

No obligation. No sales pressure. Just expert guidance to help you determine if high cash value whole life insurance is the right fit for your long-term wealth strategy.

Frequently Asked Questions

Is the Infinite Banking Concept a scam as Dave Ramsey claims?

No, the Infinite Banking Concept is not a scam. It’s a legitimate strategy using whole life insurance, which is regulated by state insurance commissioners. While not suitable for everyone, these tools offer guaranteed cash value growth, tax advantages, and flexible access to capital through policy loans.

Does cash value in whole life insurance ‘die with you’ as Dave Ramsey says?

No, this is incorrect. Cash value is not separate from the death benefit – it’s part of the total death benefit paid to beneficiaries. When you die, the full death benefit is paid out, which includes the cash value. You don’t ‘lose’ the cash value.

Are you borrowing your own money with policy loans?

No, you’re borrowing from the insurance company using your cash value as collateral. The key advantage is your cash value continues to grow as if you hadn’t borrowed anything, creating leverage without interrupting compound growth within the policy.

Do banks really use whole life insurance despite Dave Ramsey’s claims?

Yes, banks extensively use Bank-Owned Life Insurance (BOLI). According to the FDIC, U.S. banks held over $180 billion in BOLI assets as of 2020. Companies like Walmart, General Electric, and Bank of America have billions in cash value life insurance for stable returns and tax advantages.

Is ‘buy term and invest the difference’ always better than whole life?

Not necessarily. This strategy assumes people actually invest the difference consistently, ignores market risk, and overlooks tax advantages of whole life. Term insurance becomes prohibitively expensive in later years, while whole life provides guaranteed growth and permanent coverage.

Are modern whole life policies the same as ‘old school’ policies?

No, modern high cash value whole life policies designed for Infinite Banking are significantly different. They maximize cash value growth through paid-up additions, blend whole life with term insurance for optimization, and result in 70-90% lower agent commissions than traditional policies.

Do insurance agents only recommend whole life for high commissions?

This is misleading. High cash value whole life policies designed for Infinite Banking typically have 70-90% lower commissions than traditional whole life policies. Many agents recommend these policies based on their long-term benefits and client suitability, not commission structure.

Can whole life insurance really compete with mutual fund returns?

This isn’t an apples-to-apples comparison. While mutual funds may offer higher potential returns, they come with market risk and lack whole life’s benefits: guaranteed growth, tax advantages, death benefit protection, creditor protection, and the ability to use cash value as collateral for other investments.

Why do Dave Ramsey graduates need different strategies?

Dave’s advice works for people drowning in debt who need basic financial discipline. Once you’re debt-free with emergency funds, you need sophisticated wealth-building tools that provide guarantees, tax advantages, and generational wealth transfer capabilities – strategies that wealthy families actually use.

How does high cash value whole life help with real estate investing?

Policy loans provide capital for real estate without credit checks, qualification requirements, or rigid repayment terms. Your cash value continues growing while you deploy loan proceeds, creating leverage that traditional banking can’t match. Many investors use this strategy to build real estate portfolios while maintaining guaranteed policy growth.

What makes high cash value policies different from traditional whole life?

High cash value policies are specifically designed to maximize cash accumulation through paid-up additions, term blending, and flexible premium structures. They focus on banking capabilities rather than just insurance coverage, resulting in dramatically lower agent commissions and better client outcomes.

Is whole life insurance only for wealthy people?

No, high cash value whole life can work for middle-class families who have completed debt elimination and want guaranteed wealth building. However, it’s most powerful for higher-income individuals who can maximize the volume advantages and death benefit leverage opportunities.