If you’ve been researching whole life insurance, someone has probably told you that paid-up additions are “the secret” to making your policy work. They’re half right — PUAs are the single most important design lever in a whole life policy. But the way most agents explain them leaves out the details that actually determine whether your PUA strategy builds wealth or just generates commissions.

Here’s what most articles won’t tell you: the PUA ratio everyone obsesses over (80/20, 90/10) matters far less than how the policy is engineered around the PUA — the term blending, the company’s rider flexibility, the load fees, and whether the design prioritizes early access or long-term compounding. An aggressive 90/10 policy from the wrong company can underperform a balanced 80/20 from the right one over 20 years.

This guide covers what paid-up additions actually do, how to use them strategically, and where most people go wrong — including the timing decisions that nobody else in this space is talking about.

📖 Part of our Paid-Up Life Insurance series. For an overview of all four paths to paid-up status — including limited pay, single premium, dividend-driven, and reduced paid-up — see our Complete Guide to Paid-Up Life Insurance.

TL;DR — Paid-Up Additions

- Paid-up additions (PUAs) are extra premium payments that purchase fully paid-up whole life insurance, immediately increasing your cash value and death benefit

- Two ways to get them: The PUA rider (you contribute extra money) and the PUA dividend option (your dividends automatically buy more). Use both together for maximum growth

- PUAs are essential for infinite banking — without them, your policy builds cash value too slowly to function as a banking system

- The ratio isn’t everything: A well-designed 80/20 policy from the right company outperforms a 90/10 from the wrong one over the long term

- Bottom line: PUAs are the engine, but policy design is the chassis — the engine only matters if the chassis is right

Why Trust This Guide

This article is written and maintained by Barry Brooksby, authorized Infinite Banking Practitioner with 25+ years in financial services, and Steve Gibbs, estate planning attorney with 18+ years in trusts, estates, and asset protection. As independent brokers — not captive agents — we design PUA-optimized policies across every major mutual carrier and see the real-world performance differences firsthand. Insurance & Estates is ranked the #1 life insurance agency on Trustpilot with 280+ verified reviews.

Table of Contents

- What Are Paid-Up Additions?

- How Paid-Up Additions Work

- PUA Rider vs. Dividend Option — You Need Both

- How to Design a Policy Around PUAs

- When to Prioritize PUA Funding

- PUA Load Fees — What They Cost and Why They Vary

- Frequently Asked Questions

What Are Paid-Up Additions?

Paid-up additions (PUAs) are additional premium payments you make on a dividend-paying whole life insurance policy that purchase fully paid-up additional insurance coverage. Think of each PUA as a miniature whole life policy stacked onto your main policy — each one has its own cash value and its own death benefit, and each one is completely paid for the moment you buy it.

Here’s what makes PUAs different from your base premium:

Your base premium buys death benefit protection first and builds cash value slowly over many years. Most of that payment goes toward the cost of insurance in the early years, which is why traditional whole life policies take 12-14 years just to break even on cash value.

PUA payments work in reverse. After the insurance company deducts a one-time load fee (typically 4-10%), nearly all of the remaining payment goes directly to cash value. You also get a corresponding increase in death benefit, but the cash value creation is immediate — not spread over a decade.

This is why PUAs matter so much: they’re the mechanism that transforms a slow-building death benefit product into a fast-accumulating cash value asset. Without PUAs, whole life insurance is a protection tool. With properly structured PUAs, it becomes financial infrastructure.

Each paid-up addition also earns dividends, just like your base policy. Those dividends can purchase more paid-up additions, which earn more dividends, which purchase more paid-up additions — creating compound growth that accelerates over time. This is the compounding cycle that makes whole life insurance viable as a banking strategy.

PUAs are available exclusively on participating whole life policies from mutual insurance companies. Term life, universal life, indexed universal life, and variable universal life policies do not offer them.

How Paid-Up Additions Work

When you make a PUA payment, the process is straightforward:

The insurance company deducts a one-time load fee — typically between 4% and 10% depending on the carrier. The remaining amount purchases fully paid-up additional insurance. That insurance immediately increases your cash value and death benefit, begins earning dividends, and requires no future premium payments.

Here’s a simplified example of how the math works:

You pay $10,000 into your PUA rider. The insurance company deducts a 6% load fee ($600). The remaining $9,400 creates approximately $9,400 in immediate cash value and roughly $25,000-$40,000 in additional death benefit (the exact amount depends on your age and health rating — younger policyholders get a higher death benefit multiple per dollar). That $9,400 in new cash value immediately begins earning dividends alongside the rest of your policy, and those dividends will automatically purchase even more paid-up additions if you’ve selected the PUA dividend option.

Compare that to your base premium: if you pay $10,000 in base premium on a traditional whole life policy, you might see only $2,000-$3,000 in cash value by the end of year one. The rest goes toward the cost of insurance and the company’s reserves.

This is why policy design matters so much — the more of your total premium that goes toward PUAs (rather than base premium), the faster your cash value builds in the critical early years.

Key Takeaway — Why PUAs Change Everything

Without paid-up additions, a typical whole life policy takes 12-14 years to break even on cash value. With a properly structured PUA rider funded aggressively, that breakeven can be cut to 4-6 years. This is the difference between a policy that sits in a drawer and one that functions as a working financial asset. For the full picture on how PUA-optimized policies perform across the top carriers, see our 2026 ranking of the best infinite banking companies.

PUA Rider vs. Dividend Option — You Need Both

This is one of the most misunderstood distinctions in whole life insurance, and getting it wrong can cost you years of growth.

The PUA Dividend Option

Every dividend-paying whole life policy gives you choices for how to receive your annual dividend — take it as cash, use it to reduce premiums, leave it to accrue interest, or use it to purchase paid-up additions. We recommend the dividend option to purchase paid-up additions in virtually every case.

Why? If you take your dividends as cash or let them accrue interest, that income is taxable. If you use dividends to purchase paid-up additions, that money stays inside the policy’s tax-advantaged environment under IRC 7702, growing tax-deferred and accessible tax-free through policy loans. Since taxes are the single largest wealth destroyer most people face, keeping dividends inside the policy is almost always the better move.

The dividend PUA option is a standard feature of the policy — it doesn’t require a separate rider and doesn’t cost you anything out of pocket. Your dividends simply buy more insurance instead of being distributed to you.

The PUA Rider

The PUA rider is an additional feature that allows you to contribute extra money — above and beyond your base premium — specifically to purchase more paid-up additions. This is where the real acceleration happens.

Unlike the dividend option (which is limited to whatever dividend the company declares that year), the PUA rider lets you control how much additional money flows into your policy, up to the maximum allowed before triggering Modified Endowment Contract (MEC) status.

Here’s the critical detail most articles skip: you typically must add the PUA rider when your policy is first issued. Most insurance companies will not let you add it later, and even those that do may require new medical underwriting. If you’re purchasing a whole life policy and your agent doesn’t include a PUA rider, ask why — or find a different agent.

Using Both Together

When you combine the PUA rider (your voluntary extra contributions) with the PUA dividend option (your dividends automatically purchasing more insurance), you create the maximum possible compounding environment inside your policy. The rider accelerates early cash value. The dividend option ensures that growth compounds on itself year after year without any additional effort.

This is the foundation of every properly designed infinite banking policy. For a deeper look at how this fits into the full IBC strategy — including the pros, cons, and what to realistically expect — see our complete guide to the infinite banking concept.

Key Takeaway — Rider + Dividend Option = Maximum Growth

The PUA rider and the PUA dividend option are two separate features that work together. The rider lets you contribute extra money for immediate cash value. The dividend option reinvests your annual dividends to purchase more insurance tax-free. Using both together creates the compounding environment that makes whole life insurance viable as a banking and wealth-building tool.

How to Design a Policy Around Paid-Up Additions

This is where most of the internet gets PUAs wrong — and where the difference between a good policy and a great one lives.

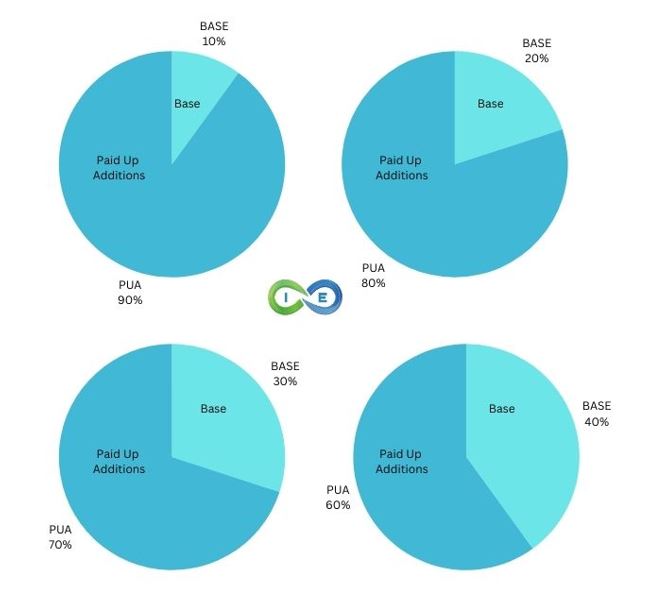

The PUA-to-Base Ratio

The most common way to talk about PUA-optimized policies is the ratio of PUA premium to base premium. Here’s how the most popular designs compare:

| PUA/Base Ratio | Ideal For | Early Cash Value | Long-Term Performance |

|---|---|---|---|

| 60/40 | Balanced death benefit + cash value | Good | Strong |

| 70/30 | Moderate cash value acceleration | Better | Strong |

| 80/20 | High early cash value + excellent long-term growth | Excellent | Excellent |

| 90/10 | Maximum immediate cash access | Superior | Varies by company |

| Best For Most IBC Practitioners | 80/20 from a top-performing company balances early cash value access with superior long-term compounding | ||

Why Higher Isn’t Always Better

Here’s the nuance most PUA articles miss: a 90/10 policy gives you more cash value in years 1-5, but it doesn’t always win over 20-30 years. The base premium is what purchases the permanent death benefit that drives guaranteed cash value growth over the life of the policy. When you shrink the base too much, you reduce the policy’s long-term growth engine.

We’ve seen this play out in real illustrations: an 80/20 policy from Penn Mutual (our #1 ranked carrier) consistently outperforms a 90/10 policy from lower-ranked companies at the 20 and 30-year marks. The early cash value difference narrows over time, and the stronger base eventually pulls ahead.

So which ratio is right? It depends on what the policy is for. If you need maximum immediate cash access — you’re deploying capital into real estate or a business opportunity within the first few years — a 90/10 design may make sense. If you’re building a long-term banking system that compounds for decades, the 80/20 sweet spot gives you excellent early access and superior long-term performance.

The Term Rider Blend

The most effective IBC policy designs incorporate a term insurance rider in the early years. The purpose isn’t the term coverage itself — it’s to raise the policy’s death benefit enough to create additional room for PUA contributions without triggering MEC status. Think of it as creating a larger container for your PUA dollars.

This term rider typically converts or falls away after 7-10 years, by which point your accumulated paid-up additions have built enough permanent death benefit to maintain the policy’s structure.

Avoiding the MEC Trap

The IRS limits how much money you can put into a life insurance policy through the Modified Endowment Contract (MEC) test. If you exceed the limit — called the 7-pay test — your policy loses its tax-advantaged loan treatment, which defeats the purpose of using whole life for banking.

The good news: your insurance company will notify you before your policy approaches MEC status, giving you time to adjust your PUA contributions. A qualified IBC practitioner designs around this limit from the start, ensuring maximum PUA funding without crossing the line. For a full explanation of MEC rules and how to avoid them, see our complete MEC guide.

Key Takeaway — Design Determines Everything

The PUA ratio matters, but the company and the practitioner designing the policy matter more. An 80/20 policy from a top-performing carrier with a skilled IBC practitioner will outperform a 90/10 from a lesser company designed by a traditional insurance agent — both in early cash value and especially in long-term compounding. For company-by-company comparisons including PUA flexibility and performance data, see our 2026 ranking of the best infinite banking companies.

When to Prioritize PUA Funding

This is the section you won’t find in other PUA articles — and it’s one of the most consequential decisions IBC practitioners face.

If you’re actively using your policy for banking (taking policy loans to fund investments, real estate, or business opportunities), you’ll eventually face this question: I have extra cash. Do I fund my PUAs or pay down my policy loan?

The instinct is to pay down the loan. It feels responsible. But the math often says otherwise.

Why PUA Funding Can Beat Loan Repayment

Every dollar you put into PUAs starts compounding immediately inside a tax-advantaged environment. That compounding continues for the entire remaining life of your policy — potentially 30, 40, or 50+ years.

Policy loans, by contrast, have flexible repayment terms. There’s no fixed schedule. The interest accrues, but it accrues against cash value that’s still growing. And in many cases, the compound growth generated by PUAs over time more than compensates for the temporary loan interest.

Here’s the key principle: policy loans are flexible, but time is not. You can always pay down a loan later. You cannot go back and capture missed compound growth.

When PUAs Should Take Priority

Expiring contribution windows. If your PUA rider has a deadline or an annual contribution window that’s about to close, fund it first. Once that window passes, you cannot go back and capture it at the same terms. Some companies will even drop the rider entirely if you don’t meet minimum contribution requirements.

Early policy years. The earlier in your policy’s life you fund PUAs, the more years of compound growth each dollar captures. A PUA dollar contributed in year 3 has dramatically more impact than the same dollar contributed in year 15.

Windfall income. Tax refunds, bonuses, inheritance, or business profits — directing this money to PUAs often produces better long-term results than accelerating loan repayment, particularly if the loan terms are flexible and you’re confident in future income to service the loan.

When Loan Repayment Should Come First

Uncertain future income. If you’re not confident you can service the loan balance going forward — career transition, business downturn, approaching retirement — reduce the loan first. Protecting the policy from excessive loan accumulation takes priority over optimizing growth.

Loan balance approaching cash value. If your outstanding loan is creeping close to your total cash value, that’s a warning sign. An overleveraged policy can lapse, triggering a taxable event. Service the loan before adding more PUAs.

Loan interest exceeding dividend crediting rate. In environments where loan rates significantly exceed what your policy is earning, the math shifts. Paying down the loan may produce better net results than funding additional PUAs — especially if you’re in a non-direct recognition policy with elevated variable loan rates.

As Barry Brooksby puts it: “The PUA-versus-loan question isn’t one-size-fits-all. If you’re confident in your future cash flow and the contribution window is closing, fund the PUA every time — you’re buying compound time you can never get back. But if the loan is creating real risk to the policy, protect the foundation first.”

Key Takeaway — Time Is the Irreplaceable Asset

PUA contribution windows close. Compound growth opportunities don’t wait. If your cash flow is stable and your policy loan isn’t threatening the policy’s health, prioritizing PUA funding typically produces superior long-term results. But never let optimization override policy safety — a lapsed policy helps no one.

PUA Load Fees — What They Cost and Why They Vary

Every insurance company charges a load fee on paid-up additions — a one-time percentage deducted from your PUA payment before the remainder purchases additional insurance. This is the only fee you’ll ever pay on a PUA; there are no ongoing charges after purchase.

Typical PUA load fees range from 4% to 10% across the major mutual carriers, with some companies reserving the right to charge up to 20% (though we’ve never recommended a company that does). The fee varies by company and sometimes by policy year — some carriers charge a higher load in year one and reduce it in subsequent years.

It’s tempting to shop for the lowest load fee and assume that’s the best deal. But PUA performance isn’t determined by the load fee alone — it’s determined by the total return of the paid-up addition over time, which includes the load fee, the dividend crediting rate, the death benefit multiple, and how efficiently the PUA compounds over 10, 20, and 30 years.

We’ve seen companies with higher load fees outperform companies with lower load fees at the 20-year mark because their dividend performance and death benefit structure more than compensated for the initial cost. The load fee is a factor, not the factor.

What matters more than the fee itself:

Rider flexibility. Can you adjust your PUA contributions up and down each year, or are you locked into a level amount? Flexible riders let you contribute more in good years and less in tight years without losing the rider entirely. Some companies will drop your PUA rider if you don’t meet minimum contribution requirements — which means losing your ability to contribute to PUAs permanently.

Dividend PUA load. Some companies charge a different (often lower) load fee when dividends purchase PUAs versus when you contribute through the rider. Some charge no explicit load on dividend-purchased PUAs — though the dividend itself may be calculated with this cost embedded.

Maximum contribution limits. Each company caps how much you can put into the PUA rider annually and over the life of the policy. These limits vary significantly and directly affect how quickly you can build your banking system.

For a company-by-company breakdown of how the top mutual carriers compare across all of these factors — including dividend rates, PUA flexibility, financial strength, and overall IBC performance — see our complete ranking of the best infinite banking companies for 2026.

How the Top Mutual Carriers Compare: PUA Rider Features

Here’s how the major mutual insurance companies structure their PUA riders across the factors that matter most:

| Company | Load Fees | Minimum Annual PUA | Best For |

|---|---|---|---|

| Penn Mutual | 10% 1st year, 6% thereafter | None (must pay 1/2 of PUA within 5 years) | Mid to long-term growth of cash value, highest retirement income |

| Mass Mutual | 10% | None (must max-fund once every 3 years) | Consistent PUA contributions, rigid and lack of flexibility |

| Guardian | 10% | $250/yr | Most flexible PUA rider with low minimum to maintain, strong early cash value |

| Lafayette Life | 6% | $120/yr | Maximum flexibility with a wide range of PUA options |

| OneAmerica | 6% | $120/yr | Average PUA growth and some flexibility |

| Foresters | 6% | $600/yr (averaged over 5-year periods) | Good PUA growth with 5-year averages and flexibility |

| New York Life | 3.5% | Must max-fund once every 3 years | Lowest load fee but rigid PUA rules, limited independent broker access (premium minimums apply) |

| Northwestern Mutual | 9% | Must match base premium payment mode | Strong long-term performance but no PUA flexibility — reductions are permanent, captive agents only |

Note: This table shows current PUA rider structures as of 2026. Northwestern Mutual is captive-only and cannot be illustrated by independent brokers. Policy designs, dividend performance, and company-specific features may significantly impact results beyond these baseline characteristics.

Beyond Paid-Up Additions: Volume-Based Banking

If the PUA discussion has you thinking about what really drives wealth inside whole life insurance, you’re asking the right questions. Paid-up additions accelerate cash value — but the real opportunity isn’t just accumulation. It’s deploying that cash value as working capital through a system designed for volume and velocity, not rate of return. That’s Volume-Based Banking — the methodology our team developed after years of implementing infinite banking and seeing what actually moves the needle.

Frequently Asked Questions

What are paid-up additions in simple terms?

Paid-up additions are extra payments you make on a whole life insurance policy that instantly create cash value and additional death benefit. Think of each PUA as a tiny whole life policy stacked onto your main policy — fully paid for in one payment, requiring no future premiums, and earning dividends from day one. The more PUAs you purchase, the faster your policy’s cash value grows and the larger your death benefit becomes. They’re the single biggest lever for turning a slow-building whole life policy into a fast-accumulating financial asset.

Do I need a PUA rider, or is the dividend option enough?

You need both. The dividend option uses your annual dividends to purchase paid-up additions — but you’re limited to whatever dividend the company declares that year. The PUA rider lets you contribute additional money on top of that, dramatically accelerating cash value growth in the early years when compounding matters most. Using the dividend option alone is like planting a garden and only using rainwater. Adding the PUA rider is turning on the irrigation system. For infinite banking, the rider is essential — it’s what gets you to usable cash value in 4-6 years instead of 12-14.

How much should I put into paid-up additions each year?

As much as you can without triggering Modified Endowment Contract (MEC) status — which is the IRS limit on how much money can go into a life insurance policy. Your insurance company and your agent should help you calculate this maximum. The MEC limit depends on your policy’s death benefit, your age, and the specific policy design. For most IBC-optimized policies, the PUA rider is designed to accept the maximum allowable contribution from day one, with a term rider blended in to create additional room. If you can’t fund the full maximum every year, that’s fine — the PUA rider is typically flexible — but contribute as much as cash flow allows, especially in the early years when compound growth has the most runway.

What happens if I stop paying into my PUA rider?

This depends entirely on the company. Some carriers have flexible PUA riders that let you reduce, skip, or resume payments without penalty. Others require a minimum annual contribution to keep the rider active — and if you don’t meet it, you lose the rider permanently. Losing the rider means losing your ability to make additional PUA contributions for the life of the policy, which is a significant loss of future growth potential. Your base policy remains in force regardless — you only need to pay the base premium to keep coverage active. But before you skip a PUA payment, check your specific company’s rider rules. This is one of the key differentiators between carriers that our Pro Client Guides evaluate when designing policies.

What are the fees on paid-up additions — and do they matter?

Insurance companies charge a one-time load fee of typically 4-10% on each PUA payment. This is deducted at the time of purchase — there are no ongoing fees after that. It’s tempting to shop for the lowest load fee, but total PUA performance over 20-30 years depends on far more than the load: dividend crediting rates, death benefit multiples, and compounding efficiency all play a role. We’ve seen companies with higher load fees outperform companies with lower fees at the 20-year mark because their overall policy performance was superior. Evaluate the total package, not just the entry cost.

Will too many paid-up additions turn my policy into a MEC?

They can, and this is the most important guardrail to understand. The IRS uses a 7-pay test to determine how much money can go into a life insurance policy within its first seven years (and after certain policy changes). If you exceed this limit, your policy becomes a Modified Endowment Contract, which means policy loans and withdrawals lose their tax-free treatment. The good news: your insurance company will notify you well before you approach MEC status, and a qualified IBC practitioner designs around this limit from the start. The term rider blend in most IBC policies exists specifically to create maximum PUA room without triggering MEC. If your agent hasn’t discussed MEC avoidance with you, that’s a red flag.

Should I fund PUAs or pay down my policy loan first?

This is one of the most consequential decisions in infinite banking, and the answer depends on your situation. If your future income is stable, your loan balance isn’t threatening the policy, and you have a PUA contribution window that’s closing — fund the PUA. You’re buying compound time you can never recover. If your cash flow is uncertain, your loan balance is approaching your cash value, or loan rates significantly exceed what your policy is earning — service the loan first and protect the foundation. The principle is straightforward: policy loans are flexible, but compound time is not. You can always pay down a loan later. You can’t go back and recapture missed PUA growth.

Can I add a PUA rider after my policy is already in force?

In most cases, no. The PUA rider should be added when the policy is first issued. Some companies may allow you to add it later, but this typically requires new medical underwriting — and if your health has changed since the original policy was issued, you may not qualify or may face higher costs. This is one of the most common and costly mistakes in whole life insurance: purchasing a policy without a PUA rider and then realizing years later that you want one. If you’re buying whole life for any purpose beyond pure death benefit protection, insist on the PUA rider at inception.

Which whole life companies have the best PUA riders?

PUA rider quality varies significantly across carriers — in terms of load fees, flexibility, maximum contribution limits, and minimum payment requirements to keep the rider active. The companies we rank highest for infinite banking tend to offer flexible riders that let you adjust contributions year to year, competitive load fees, and generous maximum limits that give you room to build your banking system quickly. Our 2026 ranking of the best infinite banking companies evaluates all of these factors across the top 10 mutual carriers, including how each company’s PUA rider performs in real-world policy illustrations.

What’s the best PUA-to-base premium ratio for my policy?

It depends on what you need the policy to do. A 90/10 ratio gives you maximum immediate cash access — ideal if you’re deploying capital into real estate or a business within the first few years. An 80/20 ratio from a top-performing company like Penn Mutual gives you excellent early access and superior long-term compounding — this is the sweet spot for most IBC practitioners building a decades-long banking system. We’ve seen 80/20 policies outperform 90/10 policies at the 20 and 30-year marks because the larger base premium drives stronger permanent death benefit growth, which in turn drives stronger guaranteed cash value growth. There is no universal “best” ratio — it’s about matching the design to your strategy. Our Pro Client Guides design custom illustrations at multiple ratios so you can compare the numbers for your specific age, health, and goals.

See What a PUA-Optimized Policy Looks Like for You

The best way to understand paid-up additions isn’t theory — it’s seeing your own numbers. Our Pro Client Guides will design custom illustrations at multiple PUA ratios from the top-performing carriers so you can compare real cash value projections, not hypotheticals.

- Custom Policy Design: Multiple PUA ratios compared side-by-side for your specific age, health, and goals

- Company Comparison: How the top carriers’ PUA riders perform differently in your situation

- MEC-Safe Maximums: Exactly how much you can contribute without triggering MEC status

- No Obligation: Complimentary session with zero pressure to purchase

Schedule Your Free PUA Strategy Session →

“One illustration with your own data is worth more than a hundred articles.” — Barry Brooksby, Authorized IBC Practitioner

Have a PUA question we didn’t cover? Drop it in the comments below — Barry and our team read every one and respond personally.

16 comments

John C

On average, dollar for dollar, how much additional life insurance does each dollar of PUA buy? Or is there a specific formula?

Steven Gibbs

Hi John, thanks for reaching out and that’s an interesting question that may be tricky to answer because PUA is for adding cash to a policy rather than specifically securing addition death benefit. Also, how much death benefit it procures may vary based upon the company that is recommended for your specific situation. I recommend that you connect with Barry Brooksby by requesting 1-1 consultation at barry@insuranceandestates.com.

Best, Steve Gibbs for I&E

Steven Gibbs is a licensed insurance agent, and the following agent

license numbers of Steven Gibbs are provided as required by state law:

Resident License; AZ agent #17508301,

Non-resident Licenses: TX agent #2273189, CA agent #0K10610,

LA agent #769583, MA agent #2049963, MN agent #40563357,

UT agent #655544.

Brenda

Is there an age requirement for any of these insurances to pay into.

Are there any insurance companies that provide coverage for 70 year old with no known medical history.

SJG

Hello Brenda, yes depending upon your health there are options for a 70 year old to get started. You can request a call from our expert Denise Boisvert by emailing her at denise@insuranceandestates.com.

Best, Steve Gibbs for I&E

Thomas Swenson

Re grammar: In at least two places, replace “then” with “than”

Insurance&Estates

Hello Thomas, I appreciate your editing feedback; however, to me, your comment is less constructive than it could be because, in a quick review, I’m not seeing where those changes are warranted. If you’d like to offer something with more detail, such as some specific corrections, I’ll look more closely at this. Interestingly, 2 of our partners are attorneys and with extensive writing backgrounds. Still, we welcome all constructive feedback and the opportunity to improve our content.

Best, Steve Gibbs, Esq., for I&E

DJ

Great content Steve, thanks!

Maybe this “then” should be “than”?

The paid up additions rider allows you to put more money into your policy then you borrowed out. This provides a great tax favored environment for your money, which also offers creditor protection depending on your state of residence.

Insurance&Estates

Thank you DJ, we appreciate all corrections and clarifications and it looks like you’re correct in this case.

Best, Steve Gibbs for I&E.

Joel

I have questions regarding different riders

Insurance&Estates

Hello Joel, I best way to get a clear idea of how to proceed is to connect with an expert. I encourage you to reach out to Barry at barry@insuranceandestates.com to schedule a call.

Best, Steve Gibbs for I&E

ELIAS NDOU

I HAVE PAID UP POLICY IN METROPOLITAN .THEN I WANT TO WITHDRAW?CAN I WITHDRAW.?

Insurance&Estates

Hello Elias, it is tough to comment on someone’s policy without looking at it directly. Feel free to reach out to Jason Herring at jason@insuranceandestates.com for personal assistance.

Best,

I&E

Steve Risk

Learning a lot, thanks.

Grammar police: in paragraph “Exclusive to whole life insurance”, there should be their. 🙂

Insurance&Estates

Thank you.