The Banking Secret They Don’t Want You to Know: The Ultimate Asset™

Table of Contents

- Introduction: The Banking Secret Revealed

- The Truth About How Banks Build Wealth

- The Ultimate Asset™: A New Paradigm in Wealth Building

- Real World Example: How The Ultimate Asset™ Changes Everything

- Eliminating Sequence of Returns Risk

- Understanding Economic Value Added (EVA)

- Asset Multiplier Blueprint

- Designing The Ultimate Asset™

- Common Misconceptions: What Most People Get Wrong

- Your Strategic Implementation Guide

- Finding the Right Professional

- Taking Control of Your Financial Future

- Frequently Asked Questions

- Guarantee your money grows every year, regardless of market conditions

- Access your capital whenever you want, without penalties

- Watch your entire account continue growing even while you’re using the money

- Build wealth completely tax-free

Sounds too good to be true? That’s exactly what I thought – until I discovered why banks and wealthy families have quietly used this strategy for over 200 years.

The Truth About How Banks Build Wealth

Here’s what fascinates me: Banks don’t follow their own advice. They don’t day trade. They don’t anxiously watch the market. Instead, they focus on something far more powerful – volume-based wealth accumulation.

The Power of Volume Over Returns

Think about how banks actually make money. When you deposit $100,000, they don’t just sit on it hoping for better returns. They leverage it to create nearly $1 million in loans. They understand that volume matters more than rate of return. They focus on how many times their money can work simultaneously.

This is where The Ultimate Asset™ changes everything.

The Ultimate Asset™: A New Paradigm in Wealth Building

Using a properly designed high cash value dividend paying whole life policy, in conjunction with an abundant mindset focused on asset acquisition, you can create a perpetual wealth-building machine that lets your money work in multiple places at once – just like banks do. Imagine having a financial foundation that offers:

Guaranteed Growth, Forever

Your money grows at a guaranteed rate every year, completely protected from market volatility. This is what makes The Ultimate Asset™ a true “sleep-easy” asset—no more sleepless nights wondering if your retirement will survive the next crash. Right now, with markets down 10-20%, even 30%, my whole life cash value is still growing, untouched by the chaos. Even better? This growth is entirely tax-free.

Here’s what makes this truly remarkable: once your money starts growing, it never stops. Unlike market-based investments where a downturn can wipe out years of progress overnight, The Ultimate Asset™ locks in your gains every year. Your cash value only moves in one direction—up. This guaranteed, uninterrupted compound growth creates a snowball effect that accelerates over time, building momentum year after year. It’s like having a financial engine that never turns off—and lets you sleep easy knowing your wealth is secure.

How The Ultimate Asset™ Performs Against Inflation

When evaluating any long-term financial strategy, one critical question remains: “Will this asset maintain its purchasing power against inflation?” This concern becomes even more relevant in today’s economic environment.

Historical Performance During Inflationary Periods

While many traditional investments struggle during inflationary periods, The Ultimate Asset™ has demonstrated remarkable stability and adaptability. Looking at historical data from major mutual insurance companies reveals an important pattern:

| Year | Average Dividend Rate | Inflation Rate | Real Return |

|---|---|---|---|

| 2005 | 6.7% | 3.4% | +3.3% |

| 2010 | 6.5% | 1.5% | +5.0% |

| 2015 | 6.0% | 0.7% | +5.3% |

| 2020 | 5.7% | 1.4% | +4.3% |

| 2024 | 5.9% | 3.2% | +2.7% |

What this data reveals is remarkable: during both high and low inflation environments, The Ultimate Asset™ has consistently delivered positive real returns (returns after accounting for inflation).

The Nelson Nash Experience

“In 1959, at the age of 28, I purchased a State Farm whole life insurance policy with an annual premium of $388. This may seem small today, but it was a significant amount for someone earning around $10,000 a year.

Fast forward to 2005, when I was 74 years old, the policy’s performance was remarkable. That year, while I still paid the same $388 premium, the guaranteed cash value increased by $800, and the dividend was $4,200 – totaling $5,000 in growth. This growth not only kept pace with inflation but significantly outpaced it.”

Why The Ultimate Asset™ Thrives During Inflation

What makes The Ultimate Asset™ particularly effective during inflationary periods?

- Interest Rate Correlation – Whole life dividend rates tend to rise during periods of higher inflation as insurance companies benefit from higher yields on their bond portfolios

- No Negative Returns – Unlike market investments that can suffer significant losses during economic transitions, The Ultimate Asset™ never experiences negative returns, protecting your previous gains

- Compounding Protection – Because there are never negative returns, you avoid the “recovery trap” where investments need substantially higher returns just to recover from losses

Consider this reality: If an investment loses 40%, it needs a subsequent 66.7% gain just to get back to even. The Ultimate Asset™ eliminates this problem entirely by locking in gains year after year.

The Recovery Trap

| Loss Percentage | Required Gain to Recover |

|---|---|

| 10% | 11.11% |

| 20% | 25% |

| 30% | 42.85% |

| 50% | 100% |

For a deeper analysis of how whole life insurance performs during different economic cycles and its relationship with inflation, read our comprehensive guide on whole life insurance performance during high inflation.

Complete Control and Access

Unlike traditional retirement accounts that lock away your money or charge penalties for early withdrawal, you maintain full access to your capital. Need money for an investment opportunity? It’s available within days, no questions asked.

The Ultimate Banker’s Secret

Here’s what makes this truly powerful – your money never stops working. When you use your capital for investments or opportunities, your entire account continues growing as if you never touched it. This is how banks multiply their money, and now you can do the same.

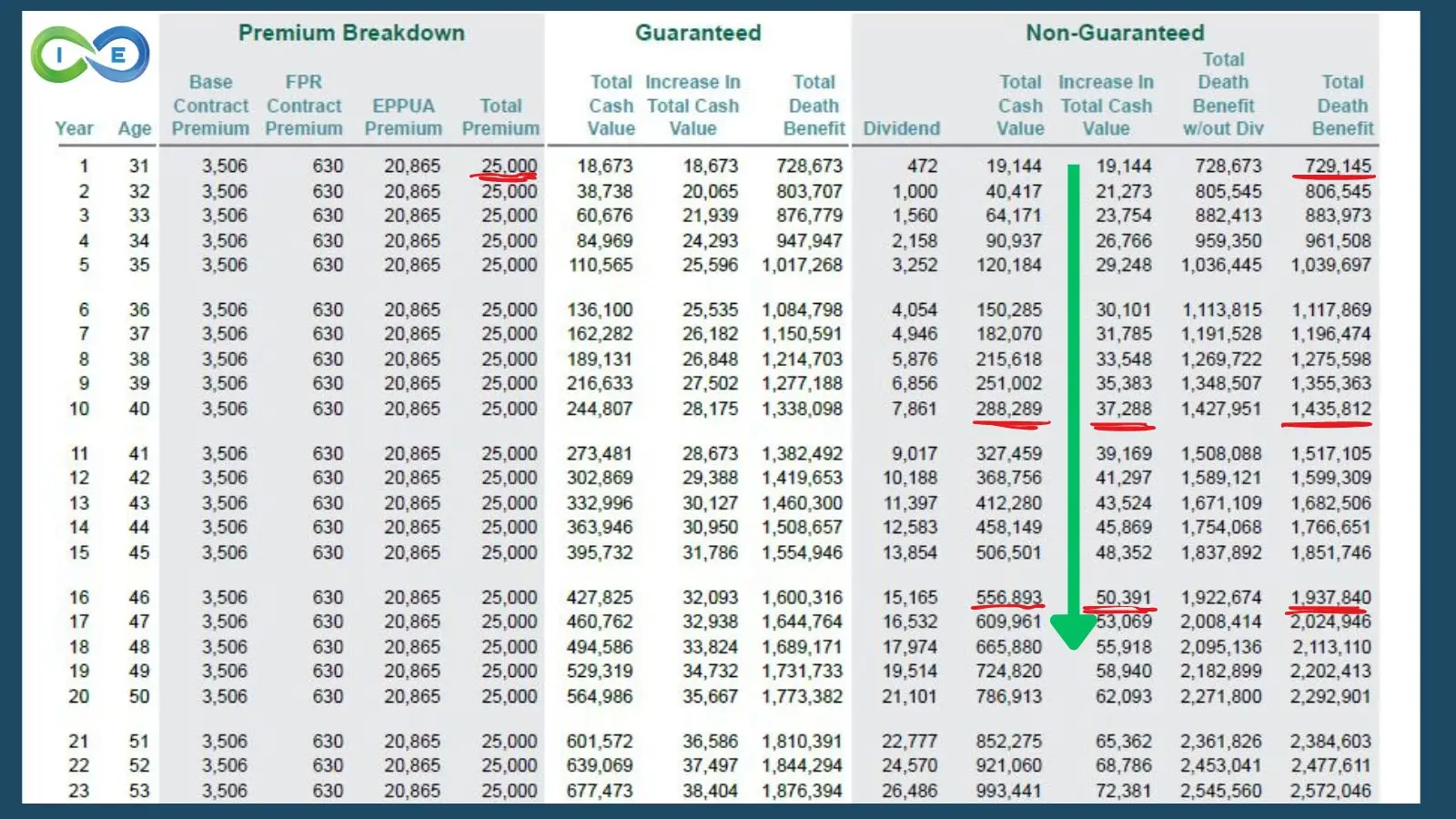

Real World Example: How The Ultimate Asset™ Changes Everything

Let me share a story about one of my recent clients – we’ll call him Ethan. Like many successful business owners, he was looking for a smarter way to build wealth for his family while keeping control of his capital.

At just 30 years old, running his own business, and with two young kids at home, Ethan understood something most people miss: True wealth isn’t just about making money – it’s about how you structure it.

How We Structured His Ultimate Asset™

We designed Ethan’s policy with a $25,000 annual premium, maximizing early cash value while maintaining the tax benefits. Here’s what happened:

From day one, his family had over $729,000 in protection. But that was just the beginning. By year 16, that protection grew to nearly $2 million – completely tax-free.

But here’s where it gets fascinating:

By year 10, something remarkable happened. His $25,000 premium was generating $37,288 in cash value growth – that’s $12,288 more than what he put in. Think about that: His money wasn’t just growing, it was multiplying.

And by year 16? His $25,000 premium was creating $50,391 in cash value growth—a cash-on-cash return of over 100%. Show me another asset that does that while maintaining complete liquidity and tax advantages.

For Ethan, his policy provides growth but it’s also a “sleep-easy” asset. If he were nearing retirement during a market crash like today’s, he could tap tax-free loans or withdrawals up to basis for income, all while his cash value keeps growing—no stress, no market panic.

Real Numbers: See how a properly structured Ultimate Asset™ grows over time. In this example, a $25,000 annual premium generates over $50,000 in cash value growth by year 16 – that’s a 100% cash-on-cash return while maintaining complete access to your capital.

Transparency: The Complete Cost Structure

Unlike traditional policies that hide costs, this illustration provides complete transparency. As you can see in Ethan’s policy breakdown:

- The $25,000 annual premium is carefully allocated: only $3,506 goes to the Base Contract Premium, with the majority ($20,865) directed to the EPPUA (Enhanced Paid-Up Additions) that accelerates cash value growth

- In the first year, Ethan’s policy generated $18,673 in guaranteed cash value, representing approximately 75% of his premium

- By year 5, his cash value reached $110,565 on $125,000 in total premiums

- Most importantly, by year 10, the annual increase in cash value ($37,288) exceeded his annual premium ($25,000) – the policy was now generating more growth each year than Ethan was contributing

This is what proper policy design looks like. It minimizes early costs and maximizes cash value from day one. While traditional whole life policies might take 15-20 years to break even, Ethan’s properly structured policy builds significant accessible capital from the beginning while still delivering the full death benefit protection of $728,673 from day one.

The Power of Strategic Design

What makes this truly powerful is how Ethan can use his growing capital. Unlike traditional investments that lock away your money or force you to sell to access capital, Ethan’s policy gives him three unique advantages:

- Tax-free borrowing against his cash value

- Continuous compound growth on his entire balance

- A growing death benefit that keeps pace with inflation

This is about protection and it’s about creating a financial foundation that works in multiple ways simultaneously. When the market dips or a real estate opportunity appears, Ethan has capital ready to deploy without disrupting his policy’s growth.

Beyond Basic Benefits

The Ultra-wealthy understand that true financial power comes from stacking multiple benefits:

- Tax-free growth and access

- Asset protection from creditors*

- Guaranteed increases every year

- Additional dividend payments from companies with 100+ year payment histories

- Complete privacy (no reporting to credit bureaus)

- A tax-efficient way to transfer wealth to the next generation

The Power of Uninterrupted Compound Growth Most people face a frustrating choice: either their money grows OR they can use it. The Ultimate Asset™ eliminates this false dichotomy. Your entire account value continues compounding even while you’re using the money for other opportunities.

*See if your state offers life insurance creditor protection.

Eliminating the Retirement Killer: Sequence of Returns Risk

For those approaching or in retirement, there’s a hidden threat that conventional financial planning rarely addresses adequately: sequence of returns risk. This risk occurs when you need to withdraw funds from your investment accounts during market downturns, forcing you to liquidate more shares to meet your income needs—permanently damaging your portfolio’s future growth potential.

The Traditional Retirement Dilemma

Imagine retiring in 2008 with $1 million in your investment accounts. The market suddenly drops 40%, reducing your portfolio to $600,000. Now you still need to withdraw $40,000 to live on:

- You’re forced to sell investments at rock-bottom prices

- You’re liquidating a larger percentage of your remaining portfolio (6.7% instead of 4%)

- Those shares can never recover in value because they’re no longer in your account

- Even when the market eventually recovers, your portfolio may never catch up

This scenario has devastated countless retirements, forcing people to drastically reduce their lifestyle or return to work.

How The Ultimate Asset™ Eliminates This Risk

With a properly structured whole life policy, this retirement nightmare scenario vanishes entirely. Here’s why:

- Borrow, Don’t Withdraw – When you need retirement income, you simply borrow against your cash value rather than withdrawing from it

- Continued Growth – Your entire cash value continues growing at the guaranteed rate plus dividends, exactly as if you never accessed the money

- Market Immunity – Market downturns become irrelevant to your income strategy, eliminating panic-driven decisions

- Flexible Repayment – You control loan repayment terms, allowing you to repay when convenient or structure it so the death benefit handles eventual repayment

This fundamental difference—borrowing against an asset that continues growing versus withdrawing from a fluctuating account—provides retirees with unprecedented financial security and peace of mind.

Think of it this way: Traditional retirement accounts force you to “cannibalize” your nest egg during bad markets, while The Ultimate Asset™ keeps your capital intact and growing regardless of market conditions. This single advantage alone can mean the difference between a stress-filled retirement constantly worrying about market performance and one where your income is reliable and predictable year after year.

Understanding Economic Value Added (EVA)

Let me share something that changed my perspective entirely about how money works. Every dollar you have is either costing you interest or earning you interest. There’s no middle ground.

The Hidden Cost of Cash

Think about it: When you spend $50,000 in cash on a down payment, you’re giving up all the compound growth and tax advantages that money could have earned. Banks understand this. That’s why they never actually spend their capital.

The Banking Reality

Here’s what fascinates me about how banks think about EVA:

- They focus on keeping their capital working in multiple places

- They understand that efficiency and volume matters more than rate of return

- They create systems where their money has multiple jobs

Your Money Should Never Stop Working

With The Ultimate Asset™, you can finally put EVA to work for you instead of against you. When you borrow against your policy:

- Your entire cash value keeps growing tax-free

- You maintain access to future capital

- Your money works two jobs simultaneously

Borrowing against your policy’s cash value isn’t just about returns, but about never letting your money take a day off. Just like banks, you can keep your capital working for you continuously, creating wealth in multiple places at once.

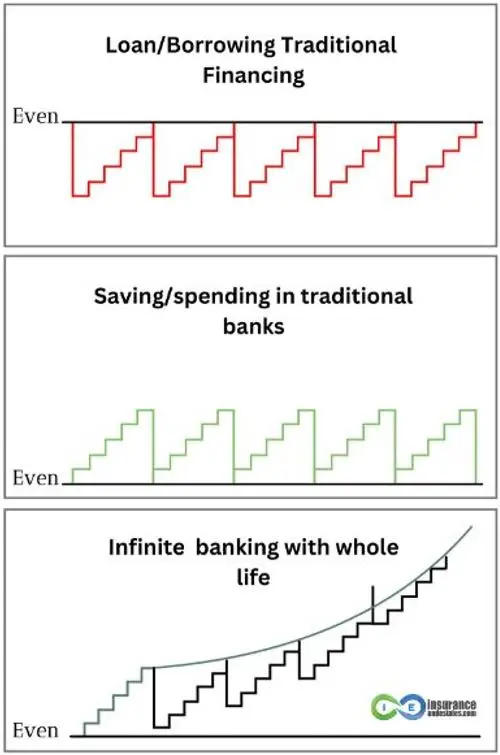

See how The Ultimate Asset™ lets you grow wealth in two places at once, unlike traditional financing methods

The Cash Method: Back to Zero

When you use cash, the story is simple. You save $50,000 for a down payment on a rental property. Once you spend it, that money stops working for you. Sure, you have the property, but the $50,000 you saved is gone – back to zero.

The Loan Method: Pay to Get Even

If you take out a traditional loan, you’re actually moving backwards. You borrow $50,000 from a bank, and spend years making payments with interest just to get back to even. All while the bank makes money on your effort.

The Ultimate Asset™ Method: Growth in Two Places

But what if you could keep your money growing while using it at the same time? This is where The Ultimate Asset™ changes everything.

Here’s how it works:

- Your $50,000 sits in your high cash value whole life policy, growing tax-free with guaranteed returns

- You borrow against this cash value to buy your rental property

- Your entire $50,000 continues earning compound interest and dividends, exactly as if you never touched it

- The rental property generates income to pay back your policy loan

- You end up with both the property AND your growing cash value

Think about that: Instead of going back to zero or paying to get even, you’re building wealth in two places simultaneously. This is exactly how banks multiply their money – and now you can do the same with the Asset Multiplier Blueprint.

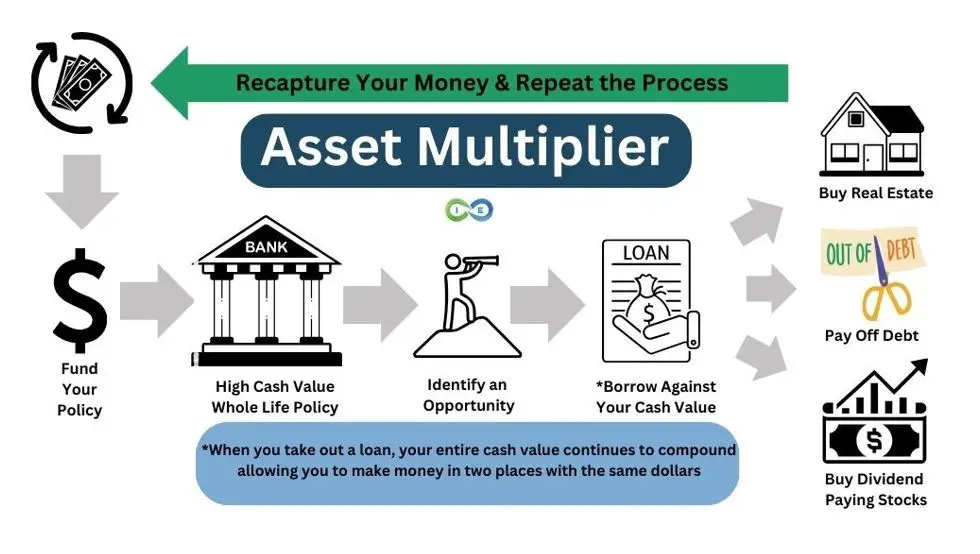

Asset Multiplier Blueprint Using The Ultimate Asset™

Here is a visual showing the Asset Multiplier Blueprint that shows how to use the Ultimate Asset to buy more assets. Then wash, rinse, and repeat.

The Asset Multiplier Blueprint: How to use your policy’s cash value to acquire assets while your money keeps growing

Designing The Ultimate Asset™

The Power of Proper Structure

Most people misunderstand what makes The Ultimate Asset™ so powerful. The key is how you structure it. The ultra-wealthy use specific design elements that transform this from a simple financial tool into a sophisticated wealth-building machine. Think of it like building a high-performance engine. Every component matters. The wealthy focus on:

Maximum Early Cash Value

Instead of waiting decades for benefits, proper structure provides significant accessible capital within the first few years. The focus is on strategic design. We want to prioritize cash value accumulation and minimize the death benefit. This is done by adding certain riders to the policy, mainly a paid up additions rider and a term rider.

Optimal Premium Structure

By using advanced funding techniques, you can maximize growth while maintaining flexibility. No more being locked into rigid payment schedules or sacrificing performance. Instead, you will have a minimum and maximum premium amount you can pay into your policy, that will vary greatly, providing maximum premium flexibility.

Tax-Free Leverage

The wealthy understand that accessibility without tax consequences creates true financial freedom. Your money grows tax-free, and you can access it tax-free. Take out a policy loan and use it to buy other assets, while your entire cash value balance still earns interest and dividends as if you never touched it.

Avoiding Modified Endowment Contracts (MECs)

A crucial aspect of properly structuring your Ultimate Asset™ is ensuring it doesn’t cross into Modified Endowment Contract (MEC) territory. A MEC is what happens when you put too much money into a life insurance policy too quickly according to IRS guidelines.

Why this matters:

- Once a policy becomes a MEC, you lose the tax-free loan access that makes The Ultimate Asset™ so powerful

- Policy loans from MECs are taxed as ordinary income to the extent there is gain in the policy

- MECs may also incur a 10% penalty for withdrawals before age 59½

A qualified advisor will carefully design your policy to maximize cash value while staying below MEC thresholds, finding the optimal balance between funding and tax advantages. They’ll also help adjust your premium payments over time to maintain non-MEC status even as your financial situation changes.

For a deeper understanding of MECs and how they affect whole life policies, read our comprehensive guide on Modified Endowment Contracts.

Common Misconceptions: What Most People Get Wrong

You can see our comprehensive list of commonly asked question and objections. Here are a few of the most common:

“Whole Life Insurance Is Too Expensive”

But what does “too expensive” really mean? Unlike term insurance that becomes prohibitively expensive as you age, The Ultimate Asset™ locks in your costs forever. More importantly, it’s not about cost – it’s about what you get in return. When properly structured, your premium builds a foundation of guaranteed growth and tax-free access that no other asset can match.

“The Returns Are Too Low”

Banks don’t stockpile $130 billion of low-return assets. In a properly structured policy, you typically see returns around 5% – tax-free. But here’s what most people miss: rate of return is only part of the equation. It’s also about:

- Guaranteed growth regardless of market conditions

- Tax-free accumulation and access

- The ability to use your money while it continues growing

- Additional dividend payments from century-old companies

“You’re Locked Into High Premiums”

This is perhaps the biggest myth. With proper structure, you maintain complete flexibility. You can adjust your premiums between a minimum and maximum range, while your money continues growing. For example, we recently designed a policy for a 30 year old where the minimum monthly payment was as low as $500, with a maximum as high as $5,000. That is a ton of flexibility.

“It Takes Too Long to Access Your Money”

Another misconception that comes from looking at traditional policies. In a properly structured Ultimate Asset™, you can access your capital within the first month. By year 3-4, many policies have cash value equal to premiums paid. Compare this to retirement accounts that lock away your money for decades. And by year 10, you could be getting an internal return that is much higher than your premium payment.

From our example above, we did a policy recently that had $25,000 annual premiums but in year 10 the cash value grows $37,000. And by year 16, the premium due is $25,000 but the cash value growth is over $50,000, providing a cash on cash return of over 100%.

“Only Insurance Agents Promote This”

Look at who actually owns these policies:

- Major banks holding over $130 billion

- Fortune 500 companies

- Wealthy families who’ve used this strategy for generations

- Sophisticated investors seeking tax-free growth

And at I&E, we design these policies so that they accumulate the most cash value with the lowest commissions. Proper policy design is not about getting your agent rich, but providing you with the best policy based on your goals.

“Infinite Banking Requires Too Much Discipline”

Infinite Banking works best with discipline because repaying policy loans ensures your cash value and death benefit grow. Skip repayments, and you might reduce your death benefit, missing the recapture phase. But here’s the “sleep-easy” part: unlike market investments, your principal never shrinks, and you set your own terms. There’s no risk of losing everything in a crash—just steady growth you control.

“Buy Term and Invest the Difference (BTID) Is a Better Choice”

BTID sounds good, but less than 2% of term policies ever pay out—most people just throw premiums away. And “invest the difference”? Most don’t, and those who do face market volatility, fees, and future tax uncertainty. The Ultimate Asset™ gives you a guaranteed death benefit, tax-free cash value, and peace of mind—your family’s future is secure, whether you pass at 75 or 105.

Your Strategic Implementation Guide

Foundation First

Start with as little as $500 monthly. This is the opposite of getting rich quick. It’s about building an unshakeable financial foundation that banks and wealthy families have relied on for generations.

Phase 1: Strategic Growth Phase

Your policy begins working immediately providing you with:

- Guaranteed tax-free growth

- Immediate access to capital

- Asset protection benefits

- Dividend potential from day one

Phase 2: Volume Building

As your policy grows, the volume of money you can use grows as well.

- Cash value equals premium (typically years 3-4)

- Dividend payments begin

- Multiple use of money strategies available

- Strategic leverage opportunities emerge

Phase 3: Activate Velocity

This is where everything accelerates. Use your growing capital for acquiring more assets, such as:

- Real estate acquisitions

- Business expansion

- Market opportunities

- Legacy building

Finding the Right Professional for Your Ultimate Asset™

The success of your Ultimate Asset™ strategy depends heavily on proper implementation. Not all financial professionals or insurance agents have the specialized knowledge to design these policies correctly. Here’s how to ensure you’re working with a qualified expert who can maximize your results:

Key Qualifications to Look For

1. Policy Design Expertise

Ask potential advisors to show you examples of policies they’ve designed (with personal details redacted) that demonstrate:

- Cash value to premium ratios in early years – Look for policies that show significant cash value accessibility within the first 3-5 years

- Paid-up additions rider (PUAR) structures – These riders are critical for maximizing early cash value and should be properly balanced

- Premium flexibility options – The policy should offer clear minimum and maximum premium ranges to accommodate your changing financial situation

If an agent can’t or won’t show you sample policy designs demonstrating these features, consider it a red flag.

2. Company Selection Knowledge

A qualified professional should be able to clearly explain:

- The differences between various mutual insurance companies offering dividend-paying whole life policies

- Why certain companies may be better fits for your specific situation (age, health, financial goals, etc.)

- Historical dividend performance comparisons between companies

- How different companies structure their policy loans and interest rates

- The financial strength ratings and stability history of recommended companies

Your advisor should recommend companies based on your specific needs, not just default to one provider.

3. Independent Status

Work with independent agents who can offer products from multiple insurance companies rather than captive agents representing just one insurer. This independence is crucial because:

- Different companies excel for different client profiles and situations

- Independent agents can compare policy features across multiple providers

- You get objective recommendations rather than being forced into one company’s product

- If your situation changes, they can recommend the most appropriate solutions

Ask directly: “Are you captive to one company or independent with access to multiple carriers?”

Red Flags to Watch For

Be cautious of professionals who:

- Push for a quick decision without thoroughly explaining policy design

- Cannot clearly explain how the policy avoids MEC (Modified Endowment Contract) status

- Recommend the same exact structure for everyone regardless of individual circumstances

- Focus primarily on death benefit rather than cash value accumulation

- Avoid discussing specific numbers or showing complete policy illustrations

- Can’t demonstrate a track record of designing policies specifically for the infinite banking strategy

Questions to Ask Potential Advisors

- “How many years have you been specifically designing policies for infinite banking or The Ultimate Asset™ strategy?”

- “What percentage of your practice is dedicated to this specialized approach?”

- “Can you show me before/after examples of how you’ve minimized commissions to maximize client cash value?”

- “How do you stay current with policy design innovations and company offerings?”

The I&E Advantage

At Insurance & Estates, we specialize in designing high cash value whole life policies that maximize your returns while minimizing agent commissions. Our team has designed hundreds of properly structured policies specifically for The Ultimate Asset™ strategy across multiple insurance carriers.

Unlike traditional agents who might design one or two of these policies per year, this specialized approach is our core focus. We match each client with the specific mutual company and policy structure that best fits their unique situation.

Remember: The difference between a properly structured policy and a traditional one can mean hundreds of thousands of dollars in accessible cash value over your lifetime. Taking time to find the right professional is essential to your financial success.

Taking Control of Your Financial Future

Let me share something that changed my perspective entirely. As an estate planning attorney, I watched client after client struggle with the same problem. They were successful, smart, and doing everything “right” according to conventional wisdom. Yet they felt trapped – their money either locked away in retirement accounts or exposed to market volatility.

Then I discovered what my wealthiest clients were doing differently.

Your Path to Financial Independence

The first step is a private Strategy Session. Rather than a high-pressure sales pitch, we’ll have a thoughtful conversation about:

- Where you are now financially

- What you want your money to do for you

- How to structure your Ultimate Asset™ for maximum benefit

- Specific strategies that match your goals

What You’ll Discover

During our time together, you’ll learn exactly how to:

- Design your policy for maximum early cash value

- Create tax-free income streams

- Protect your assets from market volatility

- Build a legacy for generations

And our gift to you. Grab a free copy of The Ultimate Asset™ – our comprehensive eBook that reveals exactly why high cash value whole life is the Ultimate Asset.

The Ultimate Asset™

How Whole Life Insurance Provides Predictable, Guaranteed Growth.

The Choice Is Yours

Right now, you have a decision to make. You can continue following conventional financial wisdom – locking away your money, hoping markets cooperate, and paying unnecessary taxes.

Or you can take control.

The same strategy that banks use to build billions… that wealthy families use to create lasting legacies… that sophisticated investors use to protect and grow their wealth – it’s available to you today.